Our newest Investment: Haranga Resources (ASX:HAR)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,410,000 HAR shares at the time of publishing this article. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time. Some shares may be subject to shareholder approval.

Uranium price runs only happen every couple of decades.

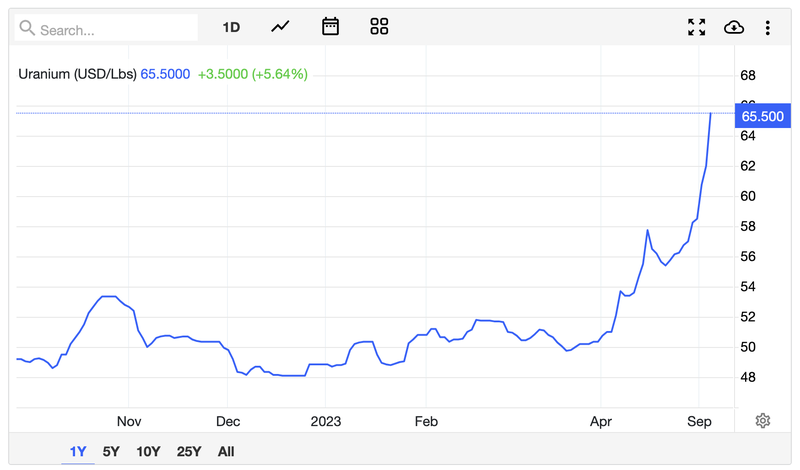

The uranium price has recently started surging, taking most uranium explorers, developers and miners with it.

The uranium price recently hit the highest it has been in over a decade and is even making it to mainstream media.

We are hoping this is finally the start of a rare multi-year uranium run - but of course, we could also be wrong, there was a “false start” uranium run back in 2020.

Our last uranium pick Okapi Resources is up over 200% over the last few weeks (past performance is not an indicator of future performance).

Introducing the latest addition to our portfolio: Haranga Resources (ASX:HAR)

Our latest Investment Haranga Resources (ASX:HAR) is a junior explorer defining a uranium project in Senegal, West Africa.

Africa is home to a host of successful uranium companies.

HAR’s project area is huge, covering 1,650km2

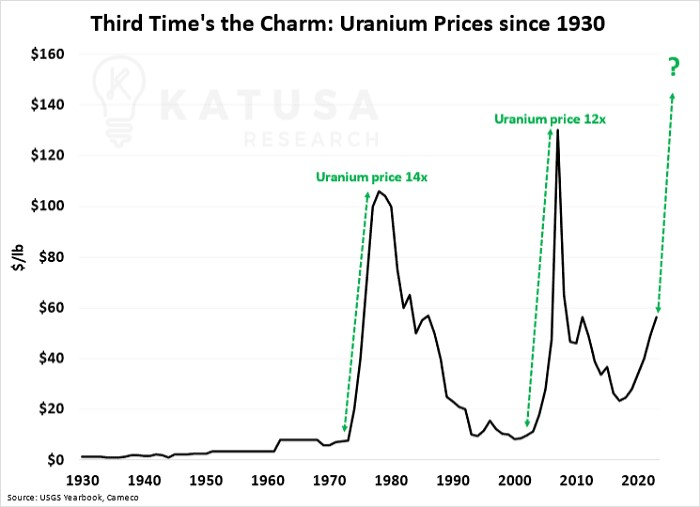

HAR’s project was previously owned by one of France’s biggest nuclear energy companies - Areva.

Not just once but twice... and both times Areva owned this project was during previous uranium bull markets - in the 1970-80’s bull market and again in the 2007-2008 bull market.

The project was last relinquished by Areva back in 2011 after the Fukushima disaster crashed the uranium price.

For major companies with many different, complex business lines, letting go of non-core projects during tough times is common.

HAR now owns this project at the start of the current uranium run.

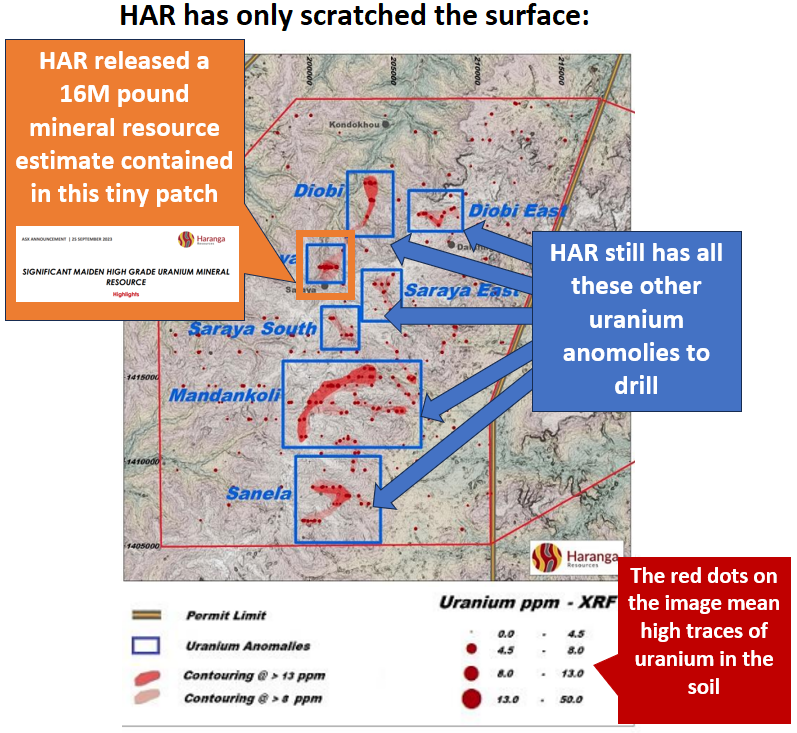

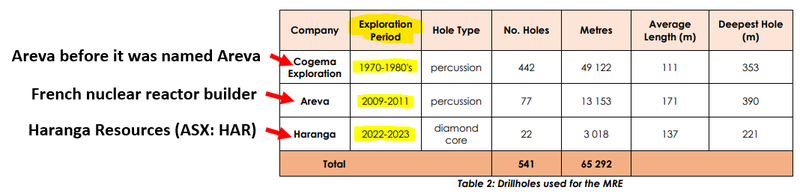

On Monday, HAR released a maiden 16m pound uranium resource estimate based on tens of thousands of meters of historical drilling done by Areva during the decades prior to Fukushima.

And the next batch of drilling is coming up as the uranium price continues to surge.

HAR has only “scratched the surface” of what we think could be a much larger uranium project.

So now that the uranium price looks to have started a run and HAR has a huge amount of other targets to go after.

We want to see HAR quickly drill out the other areas and deliver a much bigger JORC.

A few weeks ago HAR appointed just the person to do this.

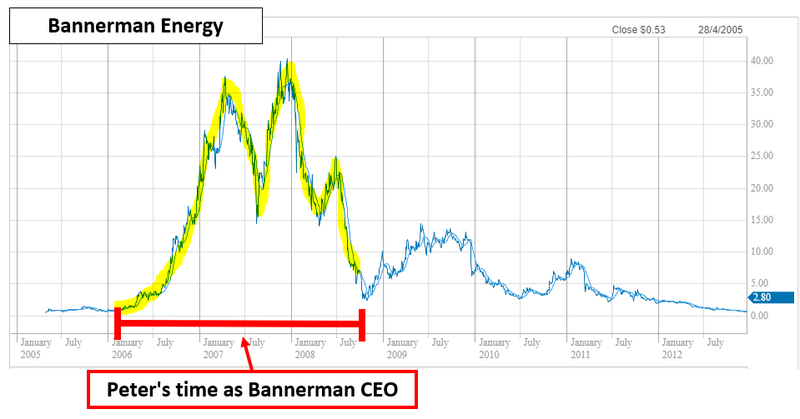

We started looking much closer at Investing when Peter Batten was appointed as HAR Managing Director earlier this month.

Peter was the founding managing director of now ~$422M Uranium (Developer) Bannerman Resources.

At Bannerman, Peter was responsible for pegging ground in Namibia where he eventually defined a JORC resource of over 100m lbs of uranium.

Under Peter’s leadership Bannerman was the best performing company on the ASX in 2006 (during the last uranium price run)

When Peter was leaving Bannerman, the company was in the feasibility study phase.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

After Bannerman, Peter did a stint at White Canyon Uranium, where he helped commercialise the company’s Utah uranium project in the USA.

Peter led White Canyon to being the first company to get a uranium mining licence in Utah in over 30 years - eventually, White Canyon was taken over by a major Canadian miner in 2011.

(Source)

Peter brings exactly what we think HAR needs at this moment in time, while the uranium price is kicking off.

Someone who can take a uranium project, build it up to a size/scale where it can be commercialised and then get the right deal done to generate value back to shareholders.

With Peter on board, we are hoping that HAR can follow Bannerman Africa’s playbook from the ~2008 uranium bull run.

Put simply, we are hoping HAR becomes Bannerman 2.0.

Right now, HAR’s project has a JORC uranium resource of 16m lbs.

The current resource sits on a tiny part of HAR’s ground next to SIX different high priority radiometric and geochemical anomalies.

Most of those anomalies are multiples the size of the one where HAR has defined its maiden resource.

For context - just one of the exploration prospects (Diobi) is ~5x the size.

We are Invested in HAR to see it drill out those prospects, multiply its JORC resource base and hopefully attract interest from major uranium buyers during what we hope will be a multi year Uranium price strength.

And we think that with his extensive experience in uranium and Africa, new HAR Managing Director Peter Batten is the person to deliver it.

Key reasons we Invested in HAR

- Uranium prices trading at decade highs - Uranium spot prices are recently trading at the highest level in over a decade. Uranium price runs don’t happen often (decades in between) and when they do happen they usually last a few years. The current Uranium run has just started.

- HAR has a giant 1,650km2 uranium exploration land holding - HAR’s project is in Senegal, West Africa. While Africa comes with risks, it is one of the rare places where massive new resources can be discovered and deliver multi-hundred million market caps uranium companies (like Paladin Energy, Lotus, Bannerman, Deep Yellow, Aura Energy).

- Nuclear giant and reactor builder Areva used to own HAR’s project... twice - The French Nuclear giant owned HAR’s project in the 70’s and ’80s, then again in 2009 to 2011 - they relinquished the project after the uranium price crashed post the Fukushima disaster. Areva did ~62,000m of drilling on HAR’s project.

- Existing 16m lbs JORC uranium resource with plenty of exploration upside - HAR’s initial resource released last week is only scratching the surface on its project. Mostly using Areva’s historical 62,000m of drilling, HAR has a further 6 anomalies covering far more ground than the initial resource yet to be tested.

- Peter Batten (Ex-Bannerman) just appointed as HAR Managing Director - Peter was one of the founding managing directors for Uranium company Bannerman Energy. In 2006, while Peter was MD, Bannerman was the best performing company on the ASX.

- Re-applying Bannerman’s African playbook, HAR to become Bannerman 2.0? - Peter was responsible for taking Bannerman’s African uranium projects from exploration into the feasibility stage. We are hoping he can do it all again with HAR.

- HAR has a tiny market cap - HAR seems to have been overlooked by the market at the start of this current uranium run, at ~15c HAR where it last traded, HAR has a ~$9M market cap.

Further down this note, we will publish our full HAR Investment Memo, which includes the objectives we want to see HAR achieve as well as the risks to our Investment thesis.

But first, a quick summary of the uranium price activity and a bit of background on the history of the project.

Why is the uranium price going up?

For those who haven’t been paying close attention to the news in recent weeks, the uranium price is flying.

(Source)

We noticed the price running a number of weeks ago, but it appears that mainstream media has now caught on.

This was a double page spread yesterday in the West Australian newspaper:

Other recently published articles:

- Why the uranium bulls are finally right (Livewire Markets)

- The Black Swan Event about to Spike Uranium —Again (Equities.com)

- Uranium price hits 12-year high as governments warm to nuclear power (Financial Times)

- Uranium is the new gold as the world goes nuclear once again (Markets Insider)

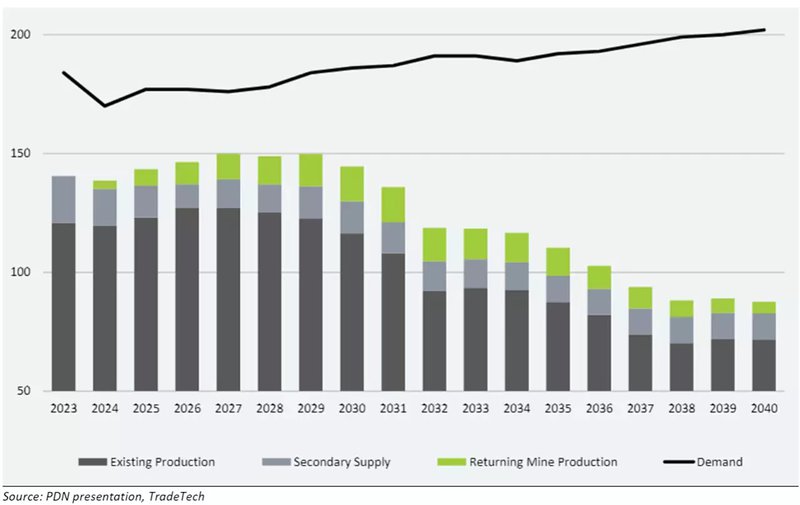

Commodity cycles are driven by supply and demand.

When demand wavers for a commodity like uranium did after the Fukushima disaster in 2011, investment in new mines dries up and supply shortages happen.

Then, when real demand grows, driven in this instance by the desire for reliable and clean base-load energy, the spot price of the commodity increases.

This is what we are seeing with the uranium price today.

We think the next decade or two will highlight the structural shortages in the uranium industry as the world embraces nuclear power:

We think this will advantage companies like HAR that have been developing its own projects ahead of time, and like it did for the players in the uranium booms of 1980s and 2008.

Uranium in the news - macro theme set for liftoff?

(Source)

(Source)

(Source)

A Look Back: The History of HAR’s Project

HAR’s project used to be owned by one of France’s biggest nuclear energy companies - Areva (recently renamed to Orano).

Areva was a French public multinational company involved in nuclear energy, including nuclear power plant design and construction, nuclear fuel supply, and nuclear services.

In its prime, the company covered all aspects of the nuclear supply chain from mining, to plant design and construction.

Even before the creation of Areva & the name change to Orano the company was actually trading as COGEMA.

Why do the Areva origins story matter to HAR?

Because HAR’s project was owned by Areva TWICE...

First as COGEMA during the 1970-80’s uranium bull market and then again a second time as Areva during the 2007-2008 bull market.

The first round of exploration done by Areva (then COGEMA) was between the 1970s and 80s uranium bull market.

At the time ~442 holes were drilled into the project, most of which was in the parts of the project where HAR has defined its initial resource estimate.

After the uranium price started coming down in the late 1980s the project was abandoned and was untouched for a period of over 20 years.

In 2007, after the uranium price started running again Areva purchased what is now the HAR project for the second time (source).

Between 2009 and 2011, Areva drilled another ~77 holes but walked away from the project after the Fukushima disaster in 2011.

It is no surprise that Areva’s exit from the project came at a time when the uranium price was trading near its lows again.

Moves in and out of exploration assets by large complex companies when spot prices fluctuate is nothing new.

As spot prices climb - exploration projects for that commodity typically become more valuable and vice versa.

And now with the uranium spot price hinting at a potential third bull market in 100 years, we think projects like HAR’s become of interest to the companies that left the space at the end of the last bull market in ~2008.

Our HAR Investment Memo:

Today, we will be launching our HAR Investment Memo, where you can find:

- Why we Invested in HAR

- Our Big Bet - what the long term upside Investment case is for HAR

- The key objectives we want to see HAR achieve

- The key risks to our Investment thesis

- Our Investment Plan

Investment Memo: Haranga Resources (ASX:HAR)

Memo Opened: 27-September-2023

Shares Held: 3,410,000

What does HAR do?

Haranga Resources (ASX:HAR) is a junior explorer defining a uranium project in Senegal, Africa.

HAR owns 70% of its Saraya project, which has an existing JORC resource of 16m Lbs uranium.

What is the macro theme?

Nuclear power has the lowest carbon footprint and highest utility rate of all renewable energy technologies.

Uranium is the primary fuel source for nuclear power, which makes it a critical mineral for a green energy future.

We expect to see uranium production increase across the world, buoyed by the transitions away from highly pollutive base-load energy generation like coal and oil.

Our long term HAR Big Bet:

“HAR re-rates to a +$100M market cap on significant resource growth and/or a transaction with a major player in the nuclear fuel supply chain”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our HAR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

The reasons we Invested in HAR

- Uranium prices trading at decade highs - Uranium spot prices are recently trading at the highest level in over a decade. Uranium price runs don’t happen often (decades in between) and when they do happen they usually last a few years. The current Uranium run has just started.

- HAR has a giant 1,650km2 uranium exploration land holding - HAR’s project is in Senegal, West Africa. While Africa comes with risks, it is one of the rare places where massive new resources can be discovered and deliver multi-hundred million market caps uranium companies (like Paladin Energy, Lotus, Bannerman, Deep Yellow, Aura Energy).

- Nuclear giant and reactor builder Areva used to own HAR’s project... twice - The French Nuclear giant owned HAR’s project in the 70’s and ’80s, then again in 2009 to 2011 - they relinquished the project after the uranium price crashed post the Fukushima disaster. Areva did ~62,000m of drilling on HAR’s project.

- Existing 16m lbs JORC uranium resource with plenty of exploration upside - HAR’s initial resource released last week is only scratching the surface on its project. Mostly using Areva’s historical 62,000m of drilling, HAR has a further 6 anomalies covering far more ground than the initial resource yet to be tested.

- Peter Batten (Ex-Bannerman) just appointed as HAR Managing Director - Peter was one of the founding managing directors for Uranium company Bannerman Energy. In 2006, while Peter was MD, Bannerman was the best performing company on the ASX.

- Re-applying Bannerman’s African playbook, HAR to become Bannerman 2.0? - Peter was responsible for taking Bannerman’s African uranium projects from exploration into the feasibility stage. We are hoping he can do it all again with HAR.

- HAR has a tiny market cap - HAR seems to have been overlooked by the market at the start of this current uranium run, at ~15c HAR where it last traded, HAR has ~$9M market.

What we want to see HAR achieve

Objective #1: Geophysical/Geochemical surveys across exploration prospects

HAR has six exploration prospects, one of which has a footprint ~5x the size of HAR’s existing JORC resource. We want to see HAR samples and run geophysics over the prospects to work out the best spots to drill.

Milestones

🔄 Geophysics/Geochemical surveys

🔄 Permitting/planning

🔲 Define drill targets

Objective #2: Drilling across exploration prospects

We want to see HAR drill at least two of its exploration prospects.

Milestones

🔲 Permitting/planning

🔲 Drilling started

🔲 Drilling results

Objective #3: Increase JORC resource

We want to see HAR multiply its existing 16m lb JORC resource.

Milestones

🔲 JORC resource upgrade commenced

🔲 JORC resource upgrade delivered

What are the risks?

Country Risk

West Africa, where HAR’s project is located, is a high-risk region of the world.

Most recently in the region there was a coup in Niger (2023), which coups in Mali (2021) and Burkina Faso (2022) in recent years.

Political instability in the region could disrupt HAR’s ability to operate or commercialise its project.

Exploration risk

HAR is planning to drill exploration targets to grow its uranium resource.

Exploration activities may or may not return any uranium mineralisation or low-grade uranium resource that is uneconomic.

Commodity risk

In recent decades, governments have shunned uranium because of the issues related waste removal and accidents like Chernobyl and Fukushima.

If the adoption of nuclear power is slower than expected then it may impact the future demand for uranium.

Uranium price risk

Share prices of junior explorers like HAR are dependent on strong spot prices for the commodity they are exploring for.

The uranium price has started running at the moment but any retracements in spot prices could lead to capital withdrawing from the sector and a fall in share prices.

Funding risk

HAR is a junior explorer with no revenues to fund exploration and ongoing costs. This means the company is reliant on capital raises to fund exploration programs.

Market risk

If the broader market sells off, investors may shy away from high-risk investment opportunities like junior explorers. During market downturns, investors will look to pull capital away from the high risk investments. HAR is a junior explorer and may be impacted by these market wide sell offs.

Our Investment Plan

As with all our exploration investments, if the share price runs in the lead up to material drilling results, or due to macro or external factors, we may de-risk by Top Slicing 20% of our position.

The rest of the Investment plan depends on the outcomes of the company’s drill campaign and will be updated accordingly, and be governed by the 2 to 3 year holding periods as defined in our trading and hold policy disclosure.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.