ASX Junior Hunting Elephant Sized Zinc and Lead Orebodies in West Africa

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Next Mining Boom presents this information for the use of readers in their decision to engage with this product. Please be aware that this is a very high risk product. We stress that this article should only be used as one part of this decision making process. You need to fully inform yourself of all factors and information relating to this product before engaging with it.

Today’s junior exploration company has just acquired a highly promising West African zinc and lead project, leveraged to the strong demand and rising prices for these commodities.

The company has agreed to acquire 100% of a promising zinc and lead exploration project in the African nation of Gabon.

Gabon is a politically stable democratic state with few instances of social instability in recent years and the government is encouraging of foreign mining activity. It has introduced specific mining investment codes which encourage investment through customs and tax incentives.

Its government is focusing on upgrading all major roads and the launch of a massive port modernisation plan that will cater for 90% of commercial traffic.

As one of the most prosperous countries in Sub-Saharan Africa, Gabon enjoys the highest Human Development Indicator (HDI) and the third highest GDP per capita in the region.

Gabon holds significant mining potential. It is a mining friendly jurisdiction, with a mature oil industry that hosts abundant energy and mineral resources with indications of mineralisation everywhere that holds the potential for real scale. However, in a win for junior explorers — including today’s company — it remains largely untested.

This prospective yet underexplored geology boasts excellent historical datasets formulated by the well renowned French Geological Survey, the BRGM (Bureau de Recherches Géologiques et Minières). And the project itself contains potential for significant, very large scale, near surface mineralisation and remains grossly underexplored.

Before we go too far, it should be noted that this is a very high-risk, speculative stock and investors should seek professional financial advice if considering this stock for their portfolio.

There is the very real potential for Tier 1 ore bodies and the company is conducting ground based geological testing in preparation for a drilling programme that’s due to begin during the second quarter of the year.

Yet this zinc and lead project is not the extent of this company’s metals arsenal. The company is exploring other frontier locations with the aim of unlocking hidden value in largely under-explored regions.

It has a diversified portfolio of exploration projects in Africa and Australia’s Northern Territory and Queensland, providing the company with exposure to various in-demand commodities including, copper, lithium and cobalt in addition to zinc and lead.

Yet, it is the Gabon project which could be the most promising as the company moves into the market at what looks to be just the right time.

Introducing,

![]()

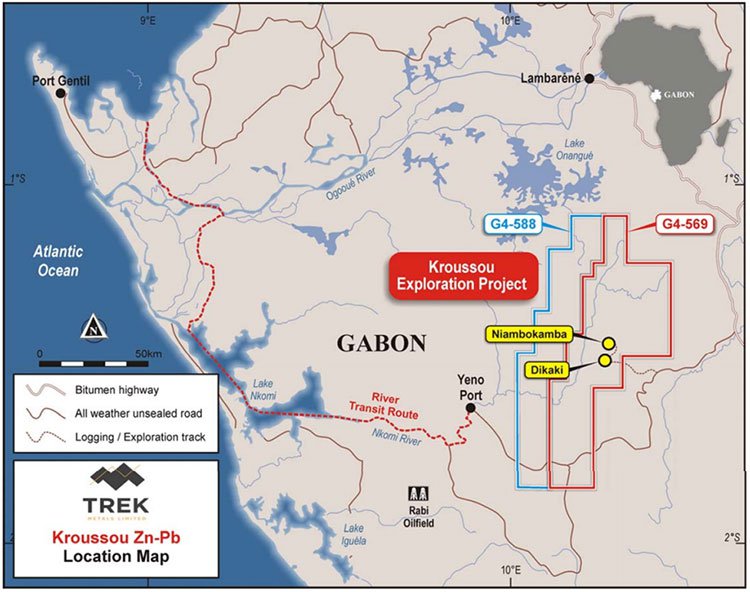

Having recently acquired the Kroussou Zinc-Lead Project in Gabon, Trek Metals (ASX:TKM) is well underway in its preparation to begin drilling in coming months.

TKM has entered into an agreement to acquire a 100% interest in the highly prospective Kroussou Zinc-Lead Project from Battery Minerals Limited (ASX:BAT) via the purchase of it’s subsidiary, Select Exploration Limited. TKM will pay BAT US$400,000 in a mix of cash and securities. It will also pay a consideration of shares and options of US$2.5 million once a Mineral Resource of 250,000 tonnes of combined zinc and lead metal is estimated at the project, as well as a smelter royalty on sales revenue.

Further details of the agreement are outlined in the company’s announcement.

Exploration from the 1960s to 1980s discovered significant zinc and lead at the Kroussou Project area and identified much near-surface base metal mineralisation.

While the project has known mineralisation, with an approximate strike length of 85 kilometres of prospective rocks, it has historically seen very little exploartion activity.

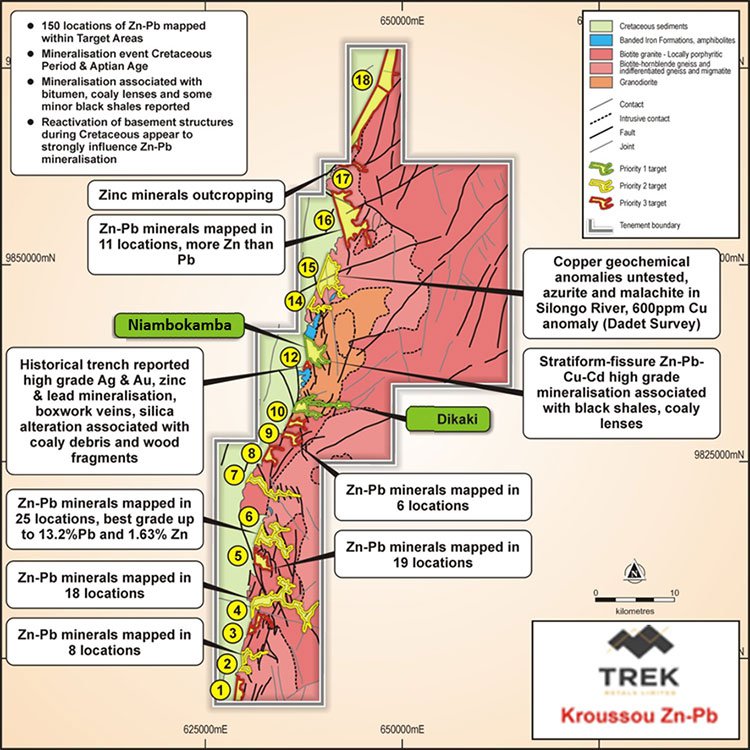

In fact, only two areas have been drilled, to a very limited extent on the entire project. These are the Dikaki and the Niambokamba areas — as seen on the map below.

Exploration to begin at Dikaki

To begin exploration, TKM selected its initial priority area, Dikaki, based on rock chips, major flexure, historical results and accessibility to the site. The Dikaki Channel has most work and it has the best access too.

About 400 very shallow holes (average depth of 16 metres) have been drilled historically at the project — at Dikaki and Niambokamba. Of all holes drilled, approximately 60% were mineralised with many terminating in mineralisation.

Previous work was focused on exploring for lead deposits within 15 metres of surface.

Drilling completed by the French Geological Survey (BRGM) at Dikaki returned many significant intercepts including:

-

8.3m

at 7.8% zinc + lead from 13.6m (ends in mineralisation) (DK040)

-

4.2m

at 4.9% zinc + lead from 3.85m and 7.0m at 8.2% zinc + lead from 9.4m (DK156)

-

1.3m

at 23.3% zinc + lead from 15.9m (DK216)

Some intervals contain narrow massive sulphide (sphalerite + galena + pyrite)

BRGM had selectively assayed where galena was abundant: sphalerite is difficult to recognise and may not have been noticed and therefore zinc rich bands may not have been assayed.

TKM’s maiden confirmation drilling identified high grade intercepts of:

-

24.7m

at 2.9% zinc equivalent from 2.0m (DKDD003)

- Including, 2.8m at 20.1% zinc equivalent from 7.7m .

-

37.1m at 2.0% zinc equivalent from 2.3m (DKDD001)

- Including 1.3m at 8.6% zinc equivalent from 11m.

- And 12.5m at 4.0% zinc equivalent from 14.5m.

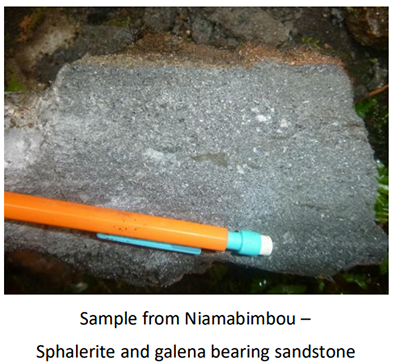

Prior to TKM acquiring the project, BAT had reported zinc and lead rich rocks including fresh sulphides at surface. These results from rock chip samples from Dikaki Prospect include:

-

9.7%

lead and 2.3% lead (ml432)

-

5.3%

lead and 1.9% lead (ml418)

-

33.1%

lead and 0.1% zinc (ml028)

-

23.2%

lead and 4.7% zinc (ml029c)

Examples of these can be seen below.

Rising commodity prices support TKM’s exploration

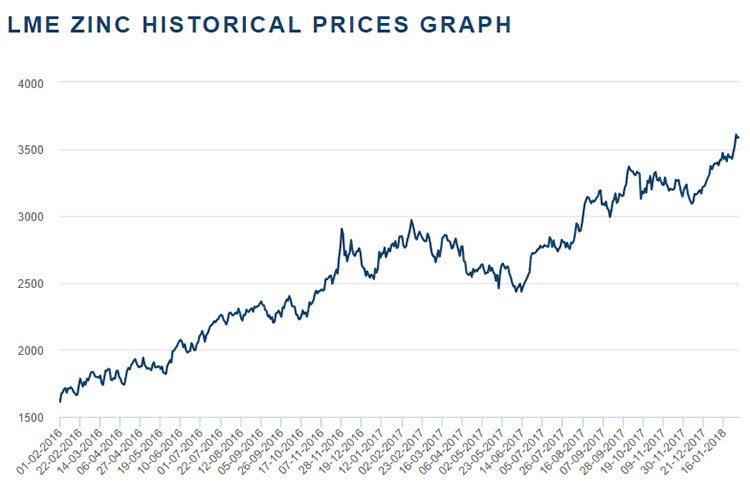

The Gabon project acquisition is timely as the zinc price is experiencing a revival. As you can see in the chart below over the past two years the zinc price has risen 123% from around US$1613/t to US$3589/t today — its highest price in more than ten years.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

While the performance is impressive, plenty of upside could still remain for zinc prices.

Of course commodity prices do fluctuate and caution should be applied to any investment decision here and not be based on spot prices alone. Seek professional financial advice before choosing to invest.

As reported in the article below, mining consultancy group, Wood Mackenzie, say the combination of scheduled mine closures, top producer Glencore's strategic production cuts, and the impact of environmental inspections in China has depleted global stocks of zinc concentrate.

During 2017, global zinc stockpiles fell by a third to 1.8 million tonnes, that’s equivalent to 47 days of global usage. By the end of the second quarter of this year, there will be less than 40 days’ of stock available for consumers, which is a critically low level that should propel prices to $4,000 a tonne by the following quarter.

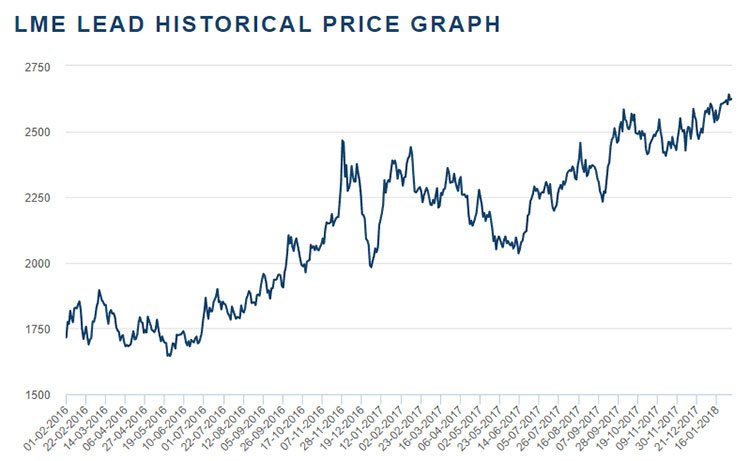

As for the lead price, it has seen a similar trend in recent years, rising from US$1715 in early 2016 to US$2623 today, for a 53% rise and its highest price in six and a half years.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Supply shortages combined with strong demand are behind the rising price. Going forward, analysts are anticipating another strong year for lead in 2018. This expectation is based on a number of factors that combine to make now an ideal time to be invested in up and coming lead producers.

Wood Mackenzie expect refined lead production to fall short of consumption this year, and don’t see the market move back into surplus until 2020.

One reason for this is that China, which is the world’s largest lead producer, imposed tough environmental regulations to fight pollution last year. This means that production at primary lead smelters will continue to be restricted by environmental regulations in 2018. A harsh winter in the United States and China has also hit current supplies.

Highly prospective, yet underexplored future metallurgy centre

In addition to the supportive commodity price environment, another factor supporting the Kroussou Project is its location.

The country of Gabon is located in an untested area of Africa, which has multiple indications of mineralisation throughout, providing the potential for real scale. It hosts highly prospective yet underexplored geology that boasts excellent historical datasets.

Along with the geographical location, the country’s government is another reason for investors in mining companies that operate in the country to be optimistic.

While its economy — and mining industry — is still developing, its mineral resources have already helped make Gabon one of the most prosperous countries in Sub‐Saharan Africa. Building on this, Gabon’s government has a vision of transforming the country into a metallurgy centre, with a dynamic fabric of small to medium sized enterprises exporting metal‐based products to the whole sub‐region and beyond.

To do this it is looking to upgrade all major roads and launch a significant port modernisation plan that will cater for 90% of commercial traffic.

TKM’s other projects

TKM’s exposure isn’t entirely tied up in its Gabon project. It also has an interest in a couple of other projects — two in Australia’s Northern Territory (a lithium and cobalt project and a copper project), and a copper project in Zambia.

Lawn Hill Project

The company currently has a large tenement holding via applications in the Northern Territory and Queensland, much of this ground subject to Native Title negotiations prior to grant.

These tenements exhibit the same geology that hosts the World Class Century Zinc Mine - (>150Mt and 10% zinc + lead).

TKM would be hoping for similar traction in the future.

Project geology can also be correlated with the rocks that host the HYC Deposit (>200Mt at 13% zinc + lead) and importantly mineral occurrences have been on the Queensland side and not on the Northern Territory side, which lacks extensive exploration.

The tenements are located along strike from the emerging Walford Creek copper-cobalt prospect.

Arunta Lithium-Cobalt Project

TKM recently acquired Elm Resources Pty Ltd which owned seven applications in the Northern Territory that are highly prospective for lithium and cobalt (six of these have now been granted). The project includes historical rock chips up to 1500ppm lithium superoxide (LiO2), 0.12% cobalt.

The acquisition provides TKM with significant exposure to strategic commodities for the mobile energy / battery market. The project includes historical reports of lithium, cobalt, tin, tungsten, copper, tantalum and niobium anomalism and/or mineralisation.

It is early stages here though and TKM has a lot of work to do so investors should seek professional financial advice if considering this stock for their portfolio.

The company’s commodity mix provides opportunities in both base load energy storage (lead and zinc) and mobile energy storage (lithium and cobalt) as the renewables sector expands globally.

Looking forward

The acquisition of the Kroussou Zinc-Lead Project armed TKM with an opportunity to grow substantially. It has a very real opportunity to discover a significant zinc-lead orebody in the mining friendly and geologically promising Gabon.

With around $2,800,000 cash in the bank and no debt, the company is in an excellent financial position to progress its exploration.

And it is backed by rising prices of both zinc and lead as the supply-demand equation is anticipated to continue to support the rising prices along with aspiring producers, such as TKM.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.