Previously Overlooked ASX Micro-Cap Confirms Transformative Tungsten Project

Published 27-MAY-2019 09:56 A.M.

|

16 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Identified by the UK, Japan, the US and Europe as a critical raw material, the specialty metal, tungsten, is seeing renewed interest amongst investors.

Tungsten has vast commercial, industrial and military applications and without it, there can be no construction, manufacturing, mining, or even touch screens. Its unique properties mean there is limited or no substitution from other metals.

Simply put, the world needs tungsten. And end users are scrambling to secure alternative, reliable sources of supply.

Non-Chinese supply is limited after attempts by China to control global supply, leaving developed and developing economies recognising that security of supply is of critical strategic importance.

As the demand for the metal rises amidst increased global competition for tungsten concentrates, so will the price and the value of the mining companies that produce it.

These dynamics mean there now exists a window of opportunity for tungsten developers to catch the attention of investors.

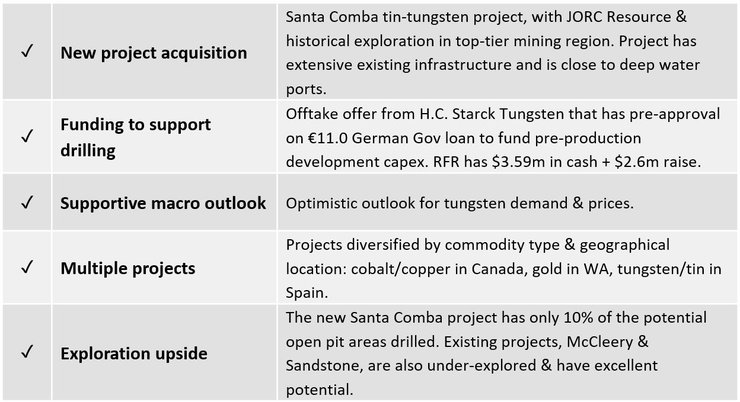

Today’s junior exploration company has recognised this and just confirmed that it is looking to acquire a 100% interest in a Spanish tungsten and tin mine.

The tungsten-tin project comes with a maiden JORC (2012) Inferred Mineral Resource completed as part of a recent scoping study, is permitted for both underground and open pit mining, and is located in a highly prospective historic tungsten and tin province. There’s also an off-take agreement potentially on the cards.

The acquisition is a transformative one for the company — an attractive tungsten opportunity with low entry costs and the prospect of great returns for shareholders.

And why do I say low entry? Well, let’s lay out the facts:

- The stock is currently unloved, capped at just $2.6 million and only very lightly traded at its current price of $0.07, (at 24 May market close).

- At cash backing its share price should be $0.13.

- The proposed transaction involves issuing shares to the vendors at $0.20 per share — vs. the current 7c share price.

- This (proposed) scrip-based purchase will also involve a capital raising targeting $2.6 million via a share placement at $0.20 per share.

Cleary there’s opportunity right now to enter the stock at a price well below what the vendors are getting issued shares at, and below the entry price of the next capital raise... Even considering dilution, this is very compelling.

Introducing,

Market capitalisation: $2.6 million

Share price: $0.07

Here’s why I like RFR:

Listing on the ASX in July last year, junior exploration company Rafaella Resources Limited (ASX:RFR) was established to explore and develop gold, cobalt, copper and other mineral opportunities.

It’s certainly getting on with the job, with a portfolio that includes the McCleery cobalt and copper project in the Yukon Territory in Canada, and the Sandstone gold project in Western Australia.

And as announced today, the company continues to expand, looking to acquire the Santa Comba tin and tungsten project in northwest Spain.

Rafaella has entered into a Heads of Agreement to acquire 100% of the shares of the private Spanish company Galicia Tin & Tungsten (GTT), owner of the Santa Comba project.

While this acquisition and progressing the Santa Comba project is RFR’s immediate focus, the McCleery and Sandstone projects also have excellent potential due to being under-explored, with limited drilling and exploration completed at the sites to date.

Firstly, let’s look at the tungsten story.

Santa Comba Tin & Tungsten Project

The Santa Comba project is located in the Spanish province of La Coruña in Galicia — a top-tier mining jurisdiction and a known rich tungsten and tin province.

The project consists of a high-grade underground deposit (Mina Carmen), a second area with potential for high-grade underground resources (Vilar), a recently discovered, extensive zone of disseminated mineralisation at surface amenable to open pit mining, and a semi-complete processing facility.

Located seven kilometres from the town of Santa Comba, the project is accessed by sealed road and is close to three deep-water port options.

Tungsten was discovered at Santa Comba as far back as 1940, but modern mining methods were not employed until 1980 when the owner, French company Coparex, carried out substantial investment and modernisation of the underground mine. It focused on the best known and developed area, Mina Carmen, and substituted the old treatment plant for a new one.

Coparex processed between 125-145ktpa of underground ore from 1982 to 1984. However, the mine closed in 1985 due to low tungsten and tin prices at that time.

In 2012, a new owner commenced construction of an updated processing plant, installing a crushing circuit (100tph) and a dense media separation plant (ca. 300tph). Yet due to financial difficulties, it didn’t recommence production at Santa Comba. GTT then acquired the project assets from the administrator in May 2015.

GTT holds 15 granted mining licences in the province that are valid to 2068, and cover the seven kilometre long Santa Comba mineralised granite massif.

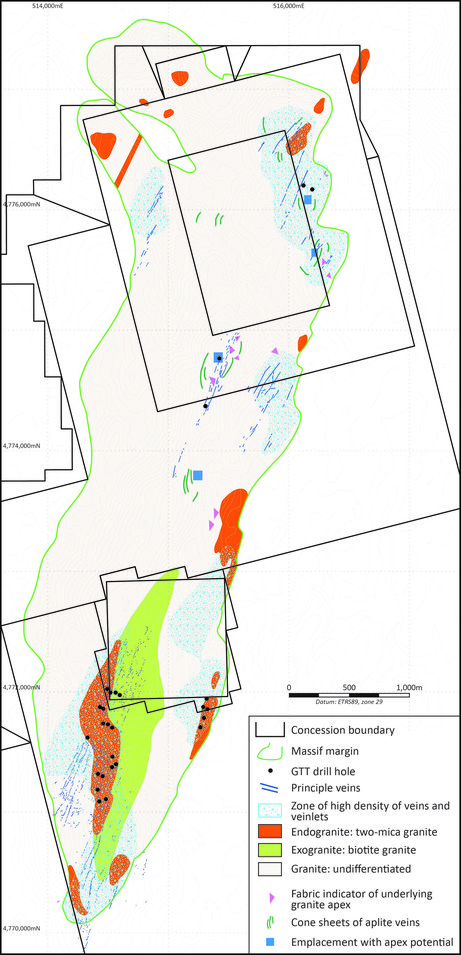

The Santa Comba granite massif has an elongated shape, extending over 7.5 kilometres in the North-South direction and a width of 1-2 kilometres. The granitic massif is not uniform, consisting of various intrusions with different facies.

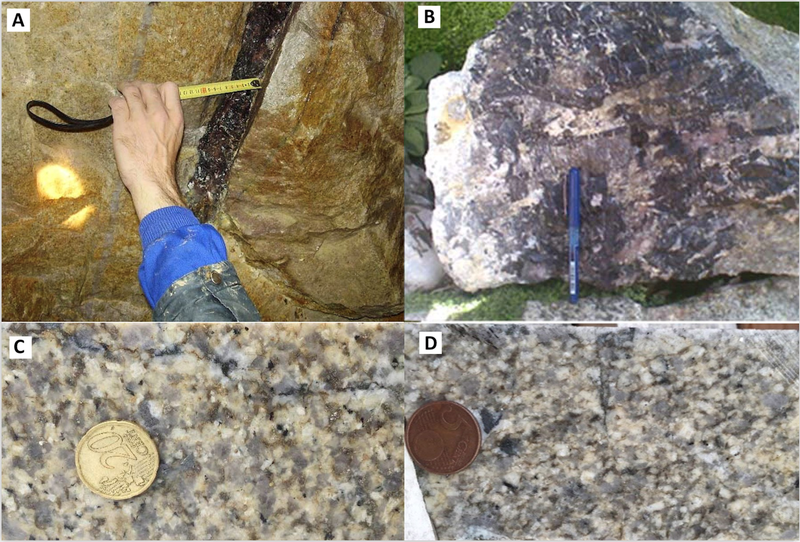

Tungsten and tin mineralisation occurs as disseminations in the granite (e.g. Quarry and Eliseo open pit prospects) and as high-grade veins (e.g. Mina Carmen, Carballeira, Santa María and Vilar underground prospects).

Here you can see the two styles of mineralisation identified at Santa Comba: vein-style and disseminated:

JORC Mineral Resource

Based on its initial scout drilling program and assessment of historical data, GTT defined maiden JORC (2012) Mineral Resource Estimates in 2016 for both near-surface disseminated and underground vein-style mineralisation.

Near-surface Resource

Inferred Mineral Resource Estimate (JORC, 2012) – near-surface disseminated mineralisation and veinlets:

Near-surface Inferred Mineral Resource reported at range of cut-off grades:

The near-surface disseminated and veinlet JORC (2012) Inferred Mineral Resource is based on 23 drill holes (2275m) conducted over less than 10% of the prospective endogranite lithology. Individual lode widths range from 2m to 30m, while 5.1 million tonnes grading an average 0.21% WO3 (0.05% WO3 cut-off) has been defined.

As part of feasibility studies, the company will assess this style of mineralisation for potential open pit mining.

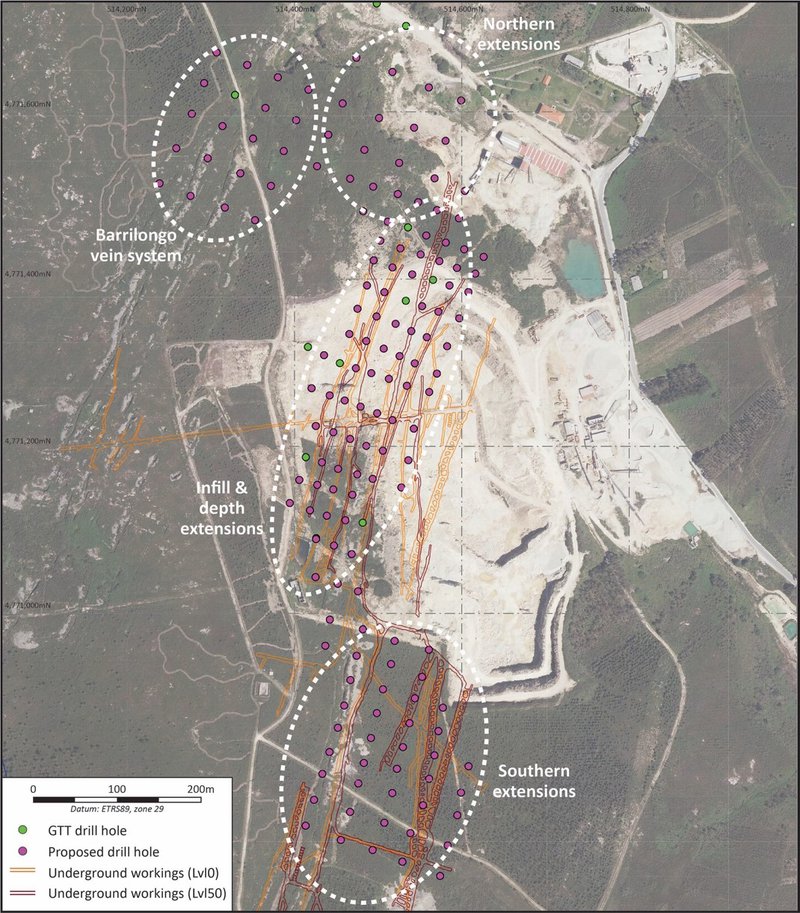

Here’s a schematic geological map of Santa Comba massif highlighting spatial extent of endogranite lithology prospective for near-surface tungsten mineralisation. Previously completed drill holes are also shown.

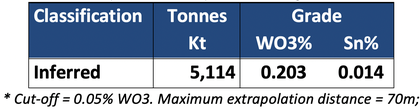

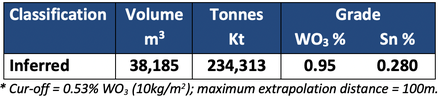

The project also hosts a high-grade, vein-hosted underground JORC (2012) Inferred Mineral Resource estimate of 234,000 tonnes at 0.95% WO3 and 0.28% Sn contained within four primary veins within the historic Mina Carmen underground mine.

However, that represents just a part of a non-JORC historical estimate completed in 1987 by previous owners. That estimate identified vein-hosted mineralisation across seven primary veins and over greater depth extensions.

Underground vein Resource

Inferred Mineral Resource Estimate (JORC, 2012) – underground veins:

Drilling and subsequent resource modelling has identified a substantial near-surface Inferred Mineral Resource.

Considerable exploration potential has been identified both along strike and at depth at the primary prospects of the Quarry and Eliseo where mineralisation is still open.

Significant tungsten mineralisation has also been identified at surface elsewhere in the massif, offering excellent potential for additional near-surface resources. These near surface prospects, potentially suitable for open pit mining, will be the main focus of a proposed Resource extension and infill drilling program.

Drilling and resource modelling has covered only a fraction of the prospective endogranite lithology, providing further encouragement for additional resource potential. Significant underground development of circa 7000m remains accessible at the project, including the large capacity primary access ramp.

Offtake agreement

The project is subject to an offer for offtake with leading global supplier, H.C. Starck Tungsten GmbH, which has obtained pre-approval for a Federal German Government Untied Loan Guarantee Scheme of up to €11.0 million (A$17.85m) to fund pre-production development capital expenditures at the project.

Once the acquisition is locked away, Rafaella plans to spend $1.3 million on a circa 8000 metre drilling campaign to upgrade the Inferred Resource and increase the overall Resource base.

The company also intends to carry out a $1 million feasibility study, as required to access the German Untied Loan Guarantee Scheme.

Rafaella currently has $3.59 million in cash, and to support the development of Santa Comba, the company has proposed a share placement aiming to raise $2.6 million at 20 cents per share.

Details of the GTT acquisition

Galicia Tin & Tungsten (GTT) is currently 75% owned by the private Australian company Biscay Minerals Pty Ltd, with the remainder held by private Spanish entity Ulex Recursos SL.

The transaction would see Rafaella issue 17.5 million shares to the vendors at 20c per share.

Once GTT achieves a JORC-compliant Resource (Measured and Indicated) of a minimum 10,000 tonnes contained WO3, grading at least 0.18%, the vendors will earn 15 million more shares.

RFR will issue a further 15 million shares to the vendors upon Santa Comba securing debt funding, subject to a mineral reserve of at least 7,000 tonnes of contained WO3.

RFR will conduct up to 30 days of final due diligence before making a final decision, which shareholders will then vote on.

Post-acquisition, two GTT representatives, Steven Turner and Robert Wrixon, will likely join the Rafaella’s Board. Turner will step in as Managing Director and relocate to Spain to ensure the project is diligently managed. Current non-executive director, Peter Hatfull will fill the Chairman’s role, replacing Graham Durtanovich.

Infrastructure

Due to significant investment by former owners, an existing processing plant is approximately 70% complete consisting of a process building, a dense media separator, jaw crusher and conveyor belts, amongst other features.

Santa Comba near term strategy

Rafaella is targeting a low cost, high margin tungsten-tin mining operation based on the shallow open pit Resource and the sunk capital expenditure.

Drilling and resource modelling has identified a substantial near-surface Inferred Mineral Resource. Considerable exploration potential has been identified both along strike and at depth at the primary prospects of the Quarry and Eliseo where mineralisation is still open.

These prospects will be the main focus of proposed resource extension and infill drilling program.

Additionally, there’s excellent potential for additional near-surface resources as significant tungsten mineralisation has been identified at surface elsewhere in the massif. Also suggesting there’s additional resource potential is the fact that drilling and resource modelling has so far covered only a fraction of the prospective endogranite lithology.

To yield similar results, the company’s peers require many times more capital expenditure. Furthermore, low development capital, easy access to near-surface resources and simple processing allows favourable operating environments irrespective of the macro conditions, which also happen to currently be supportive of the operation.

Here’s a plan view of Quarry prospect showing interpreted extensions to near-surface mineralisation:

A window of opportunity for tungsten

Demand for tungsten is now surging – as is its price. This comes down to the metal’s varied industrial uses including construction, automotive, aerospace and electronics.

This Roskill report gives an in-depth examination of market conditions.

Finfeed, recently reported on supply issues and the growth of the tungsten market:

The high density, non-corrosive, specialty metal is the hardest pure metal. It doesn’t oxidise in air, has the highest melting point and the highest tensile strength of all metals, and has the lowest coefficient of expansion.

However, global producers/developers have been massively thinned out, meaning there remain only a few serious players in the space.

Much of this had to do with an attempt earlier in the decade by China to wipe out all non-Chinese miners and dominate the production of machine tools and drill bits. However, those attempts were unsuccessful.

Currently China accounts for 85% of global tungsten concentrate supply and 50% of demand, but with the continuing reduction of concentrate exports, non-Chinese supply will become severely limited.

Adding to anticipated future demand is the fact that Europe will still produce less than half of its own tungsten requirement of 16,000tpa WO3 by 2020.

Tungsten prices firmed up nicely in the second half of 2017 and continued rising into mid-2018, providing impetus to restart work on various stalled tungsten projects.

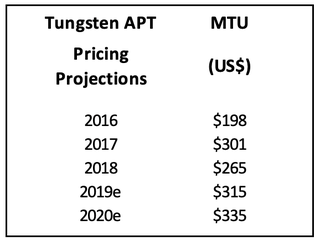

The Santa Comba underground was previously mined in commercially significant quantities between 1980 and 1985. However it became uneconomic due to low tin and tungsten prices at the time. That has now changed and the outlook for the specialty metal looks bright with prices forecast to reach US$335/Mtu by 2020.

Research and advisory group Hallgarten & Company note that, “For the first time since 2010 there now exists a window of opportunity for Tungsten developers to catch the attention of investors, as end users scramble to secure alternative, more reliable sources of supply.

“The broader economic recovery should lead to increased competition for tungsten concentrates in the global market between Chinese and non-Chinese processors and consequently resulting in an improved price structure for Tungsten and its products.

“If they accept the inevitable then a rise in the price of APT to over $300, by the end of 2019, seems like a not too outrageous postulation.”

These improved economics present Rafaella with a compelling opportunity to re-commission the Santa Comba mine. On top of that, there’s GTT’s recent discovery of the near-surface Resource at Santa Comba, suggesting significant additional low cost tonnage could be developed via open pit mining.

Other Projects

McCleery Project - Canada

The McCleery Project is located within the Yukon Territory, Canada. In exploring the project, Rafaella is focusing on the potential for it to host economic copper/cobalt mineralisation.

Initial exploration at McCleery focused on copper mineralisation, which was first discovered and staked early in 1974, with rock samples since assaying up to 15.6% copper and 461g/t silver.

Additionally, historic reports record multiple occurrences of cobalt bloom (secondary cobalt) and cobaltite (cobalt sulphide), however only one sample from the project has been assayed for cobalt, returning 0.76% cobalt and 14g/t silver.

These occurrences of cobalt bloom and cobaltite are separated by approximately one kilometre of prospective strike.

VTEM data and established copper, gold and base metal occurrences have given the Rafaella team confidence to advance exploration within the project for VMS/skarn style mineralisation.

The company is currently planning ground mapping, rock chip sampling and soils geochemistry.

Sandstone Project - WA

Rafaella’s wholly-owned Sandstone Gold Project is located 640 kilometres north-east of Perth, Western Australia within the Gum Creek Greenstone Belt. This belt is similar in structure, lithology and stratigraphy to the other greenstone belts within the Southern Cross Province of the Archaean Yilgarn Block.

The Sandstone Project is adjacent to Horizon Gold Limited’s (ASX:HRN) Gum Creek Project. Past mining and production at Gum Creek has shown widespread gold occurrence and significant potential for further discoveries.

At Sandstone, previous exploration within the project has predominantly focused on near mine exploration with work completed limited to shallow RAB drilling and soil sampling programs.

Various targets have been defined by former tenement operators, and targets include numerous historic gold workings, soil gold anomalies and RAB gold anomalies. Many of these are considered to remain inconclusively tested.

However, large areas of the project still remain essentially unexplored, whilst covering favourable structure and geology.

Rafaella plans to acquire effective geophysical, geospatial and imagery datasets over the project. Integrating this data with historical data, geology, geochemistry and field data will be used to generate conceptual targets.

Rafaella’s former target, Bonza Bore, and other promising historical anomalies are to be drill tested. Bonza Bore is historically the largest anomaly in the project area and has been proven again by the company to be of significant size.

Planning of the infill geochemistry at Bonza Bore is currently being carried out and is scheduled to be announced shortly.

Rafaella sees both the McCleery and Sandstone projects as having excellent potential due to being under-explored, with limited drilling and exploration completed at the sites to date.

Outlook

With promising copper-cobalt and gold projects in Canada and WA, plus the likely acquisition of a third asset in the Santa Comba tin-tungsten project, Rafaella offers a triple play to shareholders.

Immediate focus is on developing the newly discovered near-surface mineralisation, potentially as an open pit, and restarting the high-grade Mina Carmen underground mine. The company is targeting a low cost, high margin tungsten-tin mining operation based on the shallow open pit Resource and the sunk capital expenditure.

The acquisition of Santa Comba could certainly be a company making opportunity, given the historical exploration undertaken at the site, combined with existing Mineral Resources, along with current window of opportunity for Tungsten developers.

Given that there’s quite limited availability of high grade deposits with near term production potential, the project represents an attractive tungsten opportunity with low entry costs and the prospect of great returns for shareholders. Globally, the project economics are supported by the positive outlook for tungsten.

Plus, given RFR’s current 7 cent share price, and sub-$3 million market cap, there’s immediate opportunity on offer for early shareholders.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.