NSL Sign MoU with $86BN Indian State Government

Published 25-JAN-2016 10:23 A.M.

|

15 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

NSL Consolidated (ASX:NSL) is one of the very few miners on the Australian Securities Exchange right now, with pure exposure to India.

The Perth-based iron ore miner’s relationship with the sub-continent was reinforced recently after the company signed a Memorandum of Understanding (MoU) with the State Government of Andhra Pradesh.

The MoU unlocks significant iron ore production potential for NSL and plays directly into its five-year growth strategy plans in the region.

This is a very important deal for NSL – a small company, capped at around $6 million, is now tied formally to a large state Indian government, and is tapping into a fast growing new state, with all the momentum Prime Minister Modi can muster.

Andhra Pradesh is on track for a +14% growth for the next 15 years as a result of building a new state.

With a state GDP of $86 billion US, NSL will be there front and centre looking to capitalise on the billions of dollars of investments that will require steel production.

The basis of the MoU could position NSL to be producing in excess of 8 million tonnes per annum of iron ore in the newly formed State.

That, coupled with the recent purchase orders received from repeat customer BMM for 5000 tonnes at 55% grade, should make NSL around A$265,000 richer and places it in an excellent position moving forward.

We’ve analysed the growth prospects of this micro-cap previously, and during that time NSL has made steady progress.

NSL has diversified its product line, secured offtake and purchase orders, and generally kept things on the right track.

However, over the past couple of months we’ve also started to appreciate a key quality NSL has that you don’t usually associate with a crusty iron ore miner: diplomacy.

Key to operating in India is just how well you can play the game with the Indian government and India’s rapidly expanding business pool.

We should warn that India can be a notoriously difficult place to do business, so some caution with this investment opportunity is advised.

NSL, however, has managed to illustrate to shareholders that its efforts in setting up in India for the next five years are starting to pay off.

Doors are starting to open to new projects and new horizons...

Re-introducing:

At a broad stroke level, NSL Consolidated (ASX:NSL) plans to get its foot on low-grade iron ore and then use both wet and dry beneficiation plants pre-fabricated in China to bring it up to a higher grade which can be sold for higher prices.

We have covered NSL’s progress previously in our articles:

- Iron Ore Disruptor NSL A Step Closer to an Indian Summer

- BHP and RIO Unable to Compete: Upstart ASX Miner is the Early Mover in a Growing Domestic market

- New Revenue Streams and Magnetite Dreams for NSL

And you would now know that NSL has set up camp in the Kurnool province of Andhra Pradesh.

The plants take iron ore from NSL’s mining operations and bring it up to grade as part of your typical spoke-and-wheel operation.

Beneficiation is a strategy iron ore miners have used before to make up for low-grades in other countries like Australia and Brazil – and for NSL this technology was key to getting into India.

As a technology, it simply hasn’t taken off in India as it has in other places such as China.

As such, miners in India have gone after the low-hanging fruit of higher grades, and that makes sense for local companies.

Why waste time faffing around with beneficiation when you could just mine high-grade stuff?

For NSL though, a foreign company, it was key to securing market entry.

Business in India is littered with the corpses of many a foreign resources company trying to buy their way into the country, going for big, sexy projects.

However, NSL came in under the radar and under the noses of established Indian players to take projects the Indian miners simply weren’t all that interested in.

We humbly suggest that if NSL had swaggered into the country and set itself up as a competitor to the establishment – it probably wouldn’t have had a great time of it.

However, as a small company with the ability to pick up low-grade resources, NSL was able to manufacture a low-cost entry and build scale well beyond its station.

If the Indian iron ore community knew what NSL was up to with its canny plan, the outcome may have been different...

How to win friends and influence people

One of the big prohibitors to doing business in India is simply navigating the unwieldly and enormous bureaucracy which the country is (in) famous for.

In an interview with news site Finfeed , NSL managing director Cedric Goode said the hard yards done by NSL in being in India for upwards of five years were starting to bear fruit.

“We have this great black box of intellectual property now about what to do, when to do it, how to do it...what process to follow, how long it’s going to take and all those sorts of things,” Goode was quoted as saying.

“We’ve been through these things with complete processes at so many levels on multiple mining leases, and so things do feel like they happen a lot more quickly for us now.”

In short, NSL knows how to approach doing business in India and it’s starting to bear fruit.

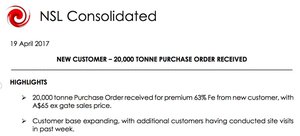

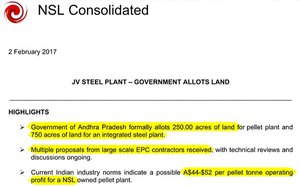

Last week, NSL told its shareholders that it had managed to secure a Memorandum of Understanding with the state of Andhra Pradesh.

It already had an MOU tied down with the state mining company, but this was above and beyond that.

Under the terms of the MOU, the government will help NSL with prompt land acquisition, adequate infrastructure development, and by offering incentives for project development.

NSL told investors that the MOU positions “NSL to be producing in excess of 8 million tonnes per annum of iron ore”.

Remember, under its current phase one and two plans it is slated to produce near to 400,000 tonnes per year.

If ever there was a statement of intent from NSL, this was it.

The deal could also see NSL construct and operate a centralised pellet plant, while NSL would set to benefit from a state government undertaking to construct a massive industrial hub just 30km from NSL’s operations .

The 28,000 acre Ovakallu Mega Industrial Hub would include access to water, power, road, and rail.

It turns out that the MOU was pretty important to shareholders, with NSL’s share price rocketing up by a third, on the back of volume of over 15 million .

Just to give you an idea, its average volume for the last 30 days (even accounting for the day’s result) was 2.7 million .

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Clearly shareholders are starting to see the fruits of NSL’s labour...

The MOU agreement came at a time when India is undergoing a great transition thanks to Prime Minister Narendra Modi.

Swimming upstream

NSL has its foot on three main iron ore upstream projects, namely being the AP23 deposit , the Mangal deposit , and the Kuja deposit .

All of these are within cooee of NSL’s phase one dry beneficiation plant at Kurnool.

AP23 deposit

This is a 73 hectare mining lease in the Kurnool district, only 13km from NSL’s existing stockyard, 5km from a national highway and 13km from rail.

While NSL hasn’t yet defined a resource at the lease, it does have some technical work under its belt with an initial exploration target of 38Mt to 95Mt with an average grade of 20-55% iron ore.

Kuja

The Kuja project has mining approval for up to 331,000 tonnes per annum of iron ore.

While this is merely an aspirational target, it gives you some idea of the sort of potential NSL sees at the project.

It has access to both established road and rail infrastructure, and links directly to the highway to the Krishnapatnam Port, which is the closest point of departure for bulk exports from Andhra Pradesh, around 330km away by road.

It’s also right next door to NSL’s beneficiation plant, where the Phase 1 production plant is located, and it is here that NSL have been refining their beneficiation capabilities.

It’s also at this site where the Phase 2 production plant will be located.

Mangal

Right next door to Kuja is Mangal, which has mining approval for 500,000 tpa over five years.

Again, NSL has infrastructure on hand, and has done technical work ups on its ore, with 213 bulk samples taken during a trial mining phase.

The material was mined, crushed and screened under the direction of geologists. It had an average grade of 38.3%, with a range between 20% and 60%.

A two-pronged attack

With the upstream taken care of, it’s time to look at how NSL plans to turn its low-grade stuff into (hopefully) high-grade profits.

Now, it is still early days for NSL, and the company will need to seal a few more deals before is operations can be deemed an outright success, so caution is advised if considering as an investment.

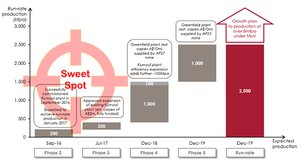

It’s planning to operate with two beneficiation plants, one constructed and producing, and the other currently being fabricated in China.

Phase one

NSL currently has a dry beneficiation plant cranking out the ore, which is bringing ore from a grade of about 20-35% and bringing it up to 50-55%, which can then be on sold to customers.

Total output from the plant is targeted at 200,000 tonnes per year, from throughput of 680,000 tonnes per year.

NSL is not producing that much yet, but it has started producing from a stock sitting at upstream permit AP23.

While it was running test mining operations at the permit back in the 2014 financial year, it managed to produce 200,000 tonnes of ore.

That ore is just...sitting there.

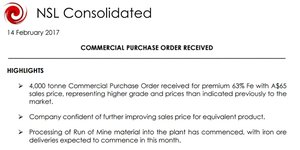

It’s from this ore that offtake agreements with BBM Ispat, which has agreed to take up to 200,000 tonnes of ore at 55%+ ore off NSL’s hands .

The Purchase Order from BMM, which is a repeat customer, was secured at the current rate of Rs 2500 (AU$53) per tonne.

NSL has managed to secure a number of purchase orders under the arrangement so far, and there’s nothing to suggest that more aren’t coming.

BMM Ispat is a massive name in Indian industry, so just securing a purchase order with these guys is huge for NSL.

It’s essentially a validation that this Australian company (in Indian eyes) taking low-grade iron ore can actually sell into the Indian market with a product good enough for BMM Ispat.

If it’s good enough for them...

Phase two

NSL’s Phase two plant is being built as a wet beneficiation plant, which is currently being built in China.

Below is one of the major components which has been completed, with only minor components now due to be built.

It will be capable of bringing low grade ore up to a grade of between 58% and 62% with a production capacity of 200,000tpa, same as the phase one plant.

However, producing a higher grade means NSL will be able to attract customers with higher grade needs than the phase one plant is capable of producing – which means a higher sale price for NSL’s product.

Commissioning is expected to take place in the second quarter and is being underpinned by two things:

The first is a $5 million investment from New York investment firm MG Partners II Ltd, and the second are offtake agreements inked with JSW Steel and BMM Ispat .

Sweet economics

One of the key selling points for NSL is that it has managed to somehow find the magic formula to keep cash costs low.

In fact, on some measures it has lower cash costs than the likes of BHP and Rio.

True, NSL has a much smaller operation, but it’s still a great result.

Below are the forecasted costs for phase one and phase two:

As you can see, cash costs at both plants come in at around A$22-A$23 per tonne.

According to analysis of costs carried out by UBS last year, the ‘total cash outgoings’ for RIO and BHP per tonne of iron ore produced was A$33 and A$32 respectively .

NSL, by setting up in India, has managed to enter a low-cost environment where the cost of pretty much everything is cheaper than it is in a lot of jurisdictions in the world.

India can be a challenging environment to work in thanks to its notorious bureaucracy (which is changing), but the trade-off is lower costs.

Hence, NSL is able to outgun the likes of RIO and BHP.

At the moment, only partial production is happening at phase one, with phase two still under construction.

However, the plan is to have both churning out 200,000 (or close to) tonnes of product per year.

If iron ore prices hold on the current path, NSL could end up churning out $10.9 million of cash flow per year.

At the time of writing, NSL has a market cap of $6.5 million ...

Of course, all the numbers above are based on forecasts, which are notoriously difficult to peg down when it comes to fluctuating commodity prices and unforeseen events, so it’s always good to seek other advice before making an investment, and that includes considering your own personal circumstances.

The above forecast doesn’t account for supplemental sales of its ‘special product’ or magnetite, which it’s exploring for at AP14.

It also doesn’t account for further opportunities NSL may have just unlocked through a mixture of charm and being in the right place at the right time...

How Modinomics is changing the game in India

One of the key reasons people may choose to invest in NSL is as a proxy for Indian growth.

Much like investors chose to invest in big iron ore miners here as a proxy for Chinese middle class growth, so too are investors seeing enormous opportunity in India.

Growth in the Indian economy means a lot more construction, and a lot more construction means more steel.

More steel, of course, means more iron ore.

Hence NSL is sitting pretty.

The reason there’s a new optimism around the Indian story is that PM Modi has a great track record in facilitating industrial growth.

To give you an example, Modi was governor of Gujurat State for about a decade. In that time he was able to turn a major deficit of $1.78 billion to a surplus of $780 million in 2012.

Better yet for commodity watchers, he made Gujurat an industrial powerhouse.

The infrastructure rating of Gujurat state is the highest in the country, and the state accounts for 17% of India’s total factory value.

In short, this is a man who knows how to get industry working – which is a refreshing change of pace for a country which has been crippled by uninspiring leadership over the past 30 years.

One of the key themes from Modi has been getting the states in India to compete for investment.

In the past, states in India have had a working relationship which is great in a lot of ways but not necessarily for business investment.

Through a number of measures (including the splitting of Andhra Pradesh state into two), he has fostered an environment where states compete for foreign investment dollars.

Hence, the states are doing things like signing huge MOU’s and making sure current investors are happy where they are.

It’s a pretty good time to be a foreign company in India. Well, better than it has been.

We should warn that progress in India is still notoriously slow, and while it’s getting better, a great deal of patience could be required from shareholders here.

One of the other key planks Modi has outlined as being key to India’s revival is a new-found focus on manufacturing.

Manufacturing growth

Modi has outlined an ambitious plan (which some analysts say is too optimistic) of making manufacturing a 25% share of GDP from its current base of 16%.

Even if India does fall short, the growth in manufacturing will have raw material suppliers such as NSL well-placed.

The Indian government has instituted a major “Make in India” campaign in order to push the Indian manufacturing sector to the next level.

Of course, with a growth in manufacturing comes a growth in steel, and therefore iron ore demand.

NSL is right there in the thick of the action.

As you can see below, current per capital estimated steel consumption for India is significantly underweight – India consumes far less steel than other countries, and it’s only a matter of time before the country catches up...

Last year the country’s Steel Ministry announced forecast growth to 2025, and those growth numbers continue.

By 2025, India is forecast to be producing 300 million tonnes of steel.

The Final Word

The premise of NSL hasn’t changed, and appears as attractive as the day we at The Next Mining Boom started covering it, particularly now with an important MoU in play.

Its game plan of sneaking in under the radar and beneficiating low-grade iron ore to a saleable grade is a canny plan if ever we’ve seen one.

It allows a company of NSL’s size to play in a bigger pond, and allows it to integrate into the Indian iron ore industry without stepping on too many toes.

It has made steady progress towards a potential doubling of its production output capacity, with commissioning of the wet beneficiation plant due in the second quarter of next year.

The market fundamentals which make NSL at least a compelling investment remain very much in play.

However, since we last covered NSL it has shown the benefit of diplomacy.

It has opened doors to that earth-shattering MOU with the Andhra Pradesh state government, which sets the scene for NSL to become something potentially huge.

Progress in India can be slow, so take that into account.

NSL, however, appears to be doing everything right at the moment.

It’s just a matter of time.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.