New revenue streams and magnetite dreams for NSL

Published 22-OCT-2015 09:59 A.M.

|

12 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

On the 25 th of September, something very interesting happened to small-cap NSL Consolidated (ASX:NSL; WKN: A0J353).

It was asked by the ASX why its shares had run up so much in a short time frame .

There wasn’t any one event which caused NSL shares to run up, so the ASX was right in asking why buyers were piling into the stock.

NSL’s answer to the regulator was simple: People are starting to buy into the NSL story.

We’ve covered NSL before in such articles as:

· BHP and RIO Unable to Compete: Upstart ASX Miner is the Early Mover in a Growing Domestic Market

· NSL Makes $230k in First Iron Ore Sale: More to Come

· NSL Now Producing: Imminent Sale of Stockpiles

We chronicled the hopes and dreams of the only pure-play Indian iron ore miner listed on the ASX, talking about its canny strategy of going after lower grade ore and then bringing it up to snuff.

We’ve talked about the burgeoning Indian iron ore market.

We’ve talked about NSL’s cash costs actually being better than the likes of Rio and BHP.

However, what we haven’t talked about is its so-called ‘mystery product’ in any great length.

While we’ll run you through the NSL gameplan and highlight the blue sky potential of this already producing ASX-listed junior, we also want to talk about the way NSL just opened up a whole new revenue stream.

By the same token, NSL is a small emerging company – and a speculative investment – investors should seek professional advice before investing.

Re-introducing:

WKN: A0J353

The new revenue stream

NSL Consolidated (ASX:NSL; WKN: A0J353) have confirmed a deal with major Indian industrial player and steel producer Sathavahana Ispat for a 4,000 tonne purchase order for NSL’s so-called ‘mystery product’ – a by-product of its iron ore mining operations, and a product relatively unique to the company.

When NSL mines for iron ore, it also brings up rocks with a unique proportion of iron, silica, and alumina.

By itself the by-product does little at all, but it can be used in blast furnaces to improve the performance of the furnace and the quality of finished cast iron when it is being produced.

Luckily for NSL, India is full of industrial players keen to improve the performance of their furnaces.

In August NSL received a trial quantity 100 tonne purchase order from Srikalahastri Pipes Limited and it has now just landed a much larger order which could end up leading to orders for 48,000 tonnes per year...

That’s somewhat of an increase on the Srikalahastri deal.

NSL tied up the initial purchase order of 4000 tonnes with Sathavanhana Ispat, under a letter of credit arrangement.

Ispat will require 4,000 tonnes per month, and while NSL was keeping mum on the chances of the 4,000 tonne order turning into a 48,000tpa deal, it’s clear that the deal will send a signal to Sirkalahastri to comer to the party or risk losing out on the product.

As the deal has been struck under a letter or credit, the value is hard to gauge although NSL did say the deal was done “with normal industry terms”.

Meanwhile, NSL also secured a purchase order for 3,000 tonnes from a “small scale steel mill”, demonstrating that there could be a market in marketing to individual steel mills on an ad-hoc basis rather than trying to tie down a big daddy purchase order.

But what is clear is the growth trajectory of sales here – from a 100 tonne purchase order in August, to a 4,000 tonne purchase order this month, to potential demand of 48,0000 tonnes per year it’s clear that the mystery product may just become an increasingly important part of the NSL’s revenue mix.

NSL’s low cost point of difference

For those of you coming to the NSL story late – there’s one crucial thing which sets NSL apart from other iron ore miners.

While every day you read about iron ore miners seeking to cut back production on the back of an ongoing weak iron ore price, NSL is seeking to expand production.

This is because NSL is able to keep cash costs very, very low.

In fact, at $23/t NSL’s cash costs are lower than that of Rio and BHP Billiton.

Somehow this small cap iron ore miner has managed to beat the big boys, who are currently doing all sorts of things to keep costs down including trialling robo-drivers for their trucks in the Pilbara.

UBS has estimated cash costs from Rio and BHP to be $34/t, which at an iron ore price of $56 for a grade of 62% means than they’re making margin of $22/t.

However, NSL’s cash costs are just $22/t to produce iron ore grading at 58% to 62%, getting a price of $57/t.

This means a margin of $35/t, which is actually better than the likes of Rio and BHP.

However, these figures are hard and fast so a note of caution should be struck.

It’s managed to keep costs low because it’s operating in India, which is a low-cost environment.

NSL has a canny plan to undercut even Indian miners...

The gameplan

The reason NSL was able to break into the Indian iron ore scene in the first place is because it’s simply mining ore the other companies won’t touch.

The Indian iron ore miners have simply gone after the super low-hanging fruit of big iron ore grades, which are more economic to process.

There’s nothing wrong with that strategy, but it creates an opportunity for a canny operator such as NSL to come along and change the game for iron ore miners in India.

NSL has managed to scoop up licenses in the country containing low grade iron ore – not normally a key selling point.

However, by bringing pre-fabricated beneficiation plants into the country it can effectively bring low-grade ore up to a point which is ready to sell to industrial users.

It already has sales underway and has several purchase orders for its product tucked neatly away.

Phase one

Phase one of the plan is a dry beneficiation plant, which is bringing iron ore at grades of between 20-35% up to 50-55%, which can then be onsold.

Total output from the plant is being targeted at 200,000 tonnes per year from throughput capacity of 680,000tpa.

Luckily, it already happened to have 200,000t of ore sitting around and has an offtake agreement penned with major industrial player BMM Ispat .

Ispat agreed back in July to take on ore from phase one with a grade of 57%, but luckily NSL had somewhat of a head-start in trying to get 200,000t to production...

While it was testing its AP23 license back in the 2014 financial year, it conducted test mining operations on a small scale to try and get an idea of how mining would work.

It ended up producing 200,000t of ore, which ended up just kind of...sitting there, until it got the phase one plant up and running and the offtake agreement inked.

As it stands, this ore is going through the plant right now, providing early cashflow as it attempts to gear up for phase two.

In fact, at full flow the plant could end up generating $3.2 million.

Phase two

Somewhere in China, a pre-fabricated wet beneficiation plant is being built right now which will provide NSL with longer term production capability, and the ability to bring ore up to a higher grade.

While the phase one plant is a dry beneficiation process, phase two will use a wet process to bring grades up to 58-62%.

Again, NSL is aiming for a plant with ultimate production of 200tpa, doubling NSL’s production capability.

While phase two is still months away from fruition, it has some compelling economics going for it.

As we showed you before, phase two will operate on a cash cost of $22/t with a plant yield of 36-37t per 100t.

It is on track to make NSL more than $500,000 per month, or $6 million per year. However it’s still early days here – NSL is a speculative stock so there is no guarantee the company will reach that milestone.

It’s all being underpinned by offtake agreements from JSW Steel and BMM Ispat which is covering the entire production run – but it remains a non-exclusive arrangement giving NSL plenty of room to try and work a better deal.

It has also been enabled by a deal struck between NSL and New York-based MG Partners II Ltd.

Back in August, MG decided to extend NSL a $5 million loan, which enabled NSL to get production happening at phase one and order the pre-fabrication unit for phase two.

MG itself specialises in investing in India, because it happens to know exactly what is going on in the country at the moment...

“Make in India”

One of the great things about India for companies seeking to work within the country is its extraordinarily low cost-base.

Consider this.

At the moment India has a GDP of about $1.3 trillion, making it the eighth largest economy in the world. However, on a ‘price parity’ basis which recognises the low cost environment of India, this rises to $3.8 trillion.

This is only behind the US and China, and if you’ve read about China lately you may want to start considering hitching your wagon to a different horse...

But it’s not just the macro factors which makes India an attractive place to do business for NSL, it is also the very real demand profile of the Indian steel market.

Given NSL is an iron ore miner, it’s well-positioned to take advantage of the growth.

An Ernst&Young report spells out the demand .

“The steel intensity curve, socio-economic indicators coupled with announced directional plans of the new Government, all indicate potential to multiply the industry size in India,” the report’s authors state.

It’s all being spurred on by the Modi government’s move to rapidly urbanise India.

“The ambitious infrastructure projects and the thrust in manufacturing through the ‘Make in India’ campaign are steps in the right direction,” E&Y noted.

“The plan for smart cities, improved road and rail connectivity by building highways, bridges and dedicated freight and superfast rail corridors have huge potential to spur domestic steel demand.”

Sounds like India is about to become China 2.0.

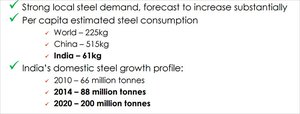

In fact, at the moment, estimated per capita steel consumption in China is 515kg per year. The world average is 225kg.

In India, it’s just 61kg, meaning that there is plenty of upside coming along for the likes of NSL to feed into.

The sentiment is backed up by the projections, in this case.

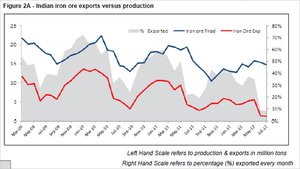

The chart above showcases a very salient point: most of the iron ore produced in India is for domestic consumption rather than export.

This means that domestic demand is strong, a fundamental NSL will be keen to play into.

After all, as a small-cap ASX-listed player it can cost a lot to set up export capacity. However, that’s not something NSL has to worry about.

It should be advised though that the Indian government can be notoriously difficult to deal with and while Managing Director Cedric Goode has a great relationship with regional government which has allowed NSL to get this far, there are still challenges and risks around operating in India, and NSL’s success is no guarantee.

Our Track Record

Did you see our article on European Metals (ASX:EMH) Electric Cars Need This: ASX Junior’s Billion Tonne Potential back in April?

Since that article was released, EMH has been as high as 250% – and it’s climbing again:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The gameplan

NSL has just outlined sales of its so-called ‘mystery product’ under a letter of credit, forming just one part of the forward plan for the company.

It’s worth stepping back and taking a look at the longer-term play for NSL:

As you can see from the above, phase one and two are only part of the plan for NSL.

Longer term its talking acquisitions to well and truly get the NSL ball rolling, while AP14 will form a central plank of its plans.

In a neighbouring province, NSL has its foot on a magnetite project which has been declared a “project of national significance”, meaning that NSL could potentially fast-track the development of the project.

The Indian government restricts projects given this classification to projects deemed critical to the national interest, or projects involving more than $180 million of total investment.

It’s clear that the Indian government thinks AP14 is a fairly big deal, but why?

The target mineralisation at AP14 consists of Banded Magnetite Quartzite, which from surface mapping and geomagnetic surveys, covers between 50% and 70% of the project area.

It has a target exploration figure of 134 million to 377 million tonnes of magnetite, at grades ranging from 25% to 50% iron.

However, within that contains potential for high grade ‘Direct Ship Ore’ enriched magnetite, with 5-10 million tonnes at 55% to 65% iron tipped.

It’s still conceptual in nature, but it screams blue sky.

Final word

NSL already had a few basic things going for it.

It was a low cost miner in a low cost environment, where demand for its product is set to increase exponentially.

However, lately NSL has started to offer a glimpse into its blue sky potential, and the latest revenue diversification should do wonders for the company.

NSL remains a small cap miner, however – so caution should be advised when weighing up whether to invest or not, and it’s always a good idea to seek professional advice.

In a matter of months, it will have the phase two plant on site and ready to rumble. Once this happens, NSL production capability will double.

In the meantime, it continues to talk to major industrial players in India about offtake agreements, giving it further confidence in its near-to-medium term plans.

They’re also being underpinned by a previously-arranged loan, meaning a dilution of shareholders will be kept to a minimum.

In the medium term, expect to hear about production ramping up at phase one, phase two being installed, potential acquisitions and its very promising magnetite project.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.