In Depth: Phosphate Price remains above highest predicted price in MNB’s scoping study

A month ago we wrote about the phosphate price surging above the highest anticipated level in MNB’s Scoping Study as countries rush to ensure food security in the wake of COVID-19.

Phosphate is used to produce fertilisers to grow food. Our investment Minbos Resources (ASX:MNB) is developing a phosphate (fertiliser) project in Angola with a 6 million tonne mining target and a 21 year mine life.

The higher the phosphate price, the higher the value of MNB’s phosphate project.

We promised a deep dive into the impact of the surging phosphate price on MNB’s project economics and here it is - these are our own calcs that we have used to support our investment decision as long term investors in MNB.

We have invested twice in the ~$40M MNB over the last 11 months, once at 3c then again in the last placement 8c - our average entry price is ~5c. We have not sold. We are long term holders and are now close to the 12 months capital gains discount on our first tranche of MNB.

We invested in MNB because their Scoping Study indicates just US$27M CAPEX will get them an after tax NPV of between $159M and US$260M, and we believe phosphate prices will continue to be strong as global food security comes into play.

This NPV of $US260M is using a phosphate price PRIOR to this year's surge... spoiler alert it’s a lot higher now.

MNB plans to mine Phosphate Rock and build a granulation plant to produce MAP (mono-ammonium phosphate).

MAP is an important source of phosphorus and nitrogen for crops and is widely used as a granular fertiliser.

MAP price surge - A US$550 million project for $40 million?

At the current MAP price, MNB shareholders own a stake in a $40 million company that is developing a project with what we calculate to be a pre-tax net present valuation of approximately US$550 million (using the MAP price sensitivity curve in the MNB scoping study page 45 and 46).

That’s at a cost of less than 10% of the NPV. A rule of thumb we use is companies at this stage should trade at about 30% to 50% of NPV.

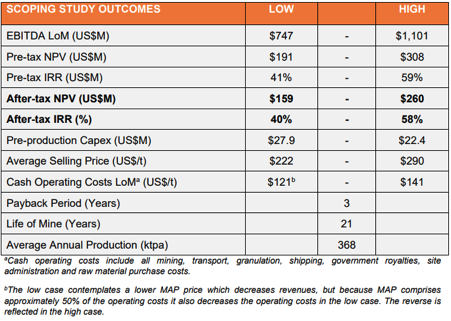

The Scoping Study estimates released by MNB in August last year pointed to a pre-tax net present value ranging between US$191 million and US$308 million with mid-range capital expenditure of US$25 million.

The following data table lists the key valuation metrics that supported the original scoping study NPV, and it is worth reading footnote ‘b’ about the MAP prices used in the calcs:

The low case contemplates a lower MAP price which would put a drag on revenues.

However, the opposite has happened.

MAP prices have soared in 2021 to a point where they are now some US$360 per tonne higher than the mid-range and US$300 per tonne higher than the high-end estimate in the base case scenario.

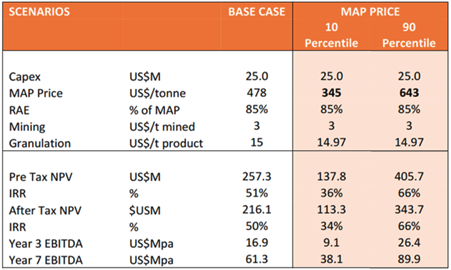

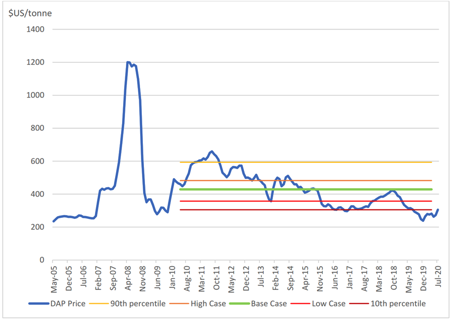

You can see MNB’s project sensitivity to MAP prices illustrated below, even though the highest MAP price (US$643 per tonne) is still well shy of the current spot price of US$780 per tonne.

At a MAP price of US$643 per tonne, the net present value leaps from the base case of US$257 million to US$405 million.

We calculate that the NPV increases even further to US$550 million based on the current MAP price of US$780 per tonne.

Based on current foreign exchange rates this equates to an NPV of A$733 million, not bad for a $40 million company (this is our rough calc, we haven’t included inflation and increased steel prices to build the plant)

If MNB were to trade in line with the high-end of the pre-tax net present valuation of approximately US$406 million, the market valuation would imply a share price of more than 80 cents.

Unfortunately company values on market don’t usually match NPV value but the rule of thumb we use for a rough valuations (of companies at the stage MNB is at) is the market cap should be around 30% to 50% of the NPV - still giving us over $200M market cap using 30% of MNB’s NPV at the current MAP price. MNB is currently capped at ~$40M.

Commodity prices rising - What is the impact on MNB’s project cost curve?

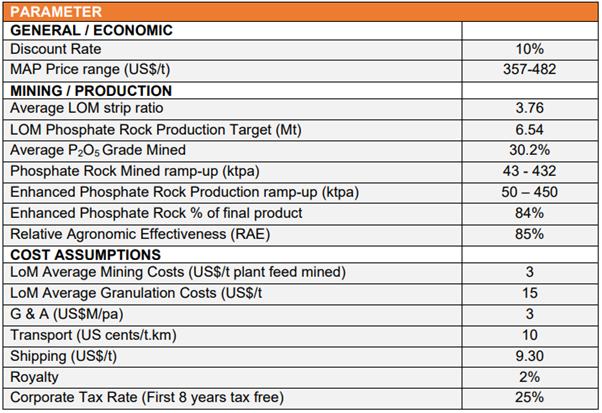

The following excerpt from MNB’s Scoping Study incorporates all production and cost factors impacting the projected economic viability.

In our discussions with MNB, management indicated that the main change in costs that is likely to be factored into the Definitive Feasibility Study (which will be a more refined update on MNB’s project) hinges around steel prices that have doubled since the Scoping Study was completed.

MNB will be producing and selling MAP, so obviously MAP prices surging is good. On the other side MNB will be using steel to build its plant and steel prices are rising too... which is not welcome news but certainly is manageable.

While this could result in a 25% increase in costs, MNB has two factors working in its favour.

Firstly, mid-range capital expenditure of about US$25 million makes this an extremely low-cost project. This is particularly relative to its sizeable NPV and the life of mine that is estimated to generate robust underlying earnings across a 21 year mine life even factoring in conservative MAP prices.

A 25% increase in capital expenditure based on the top end of cost estimates (circa US$28 million), increases capex to US$35 million.

A $7 million increase in capital expenditure almost becomes irrelevant relative to our calculated net present value of US$550 million based on the spot MAP price (US$780/tonne).

MAP price - how strong for how long?

Like any other commodity, as well as up, the MAP price also has the potential to move down. This will be driven by supply/demand dynamics, and whilst it's very hard to predict what's in store, at this stage it is difficult to see any negative headwinds emerging.

Profercy, an independent industry analysis group that focuses on global fertiliser markets, prices and trends, estimated that the MAP price was in a range between US$780 and US$790 as at 17 June, 2021.

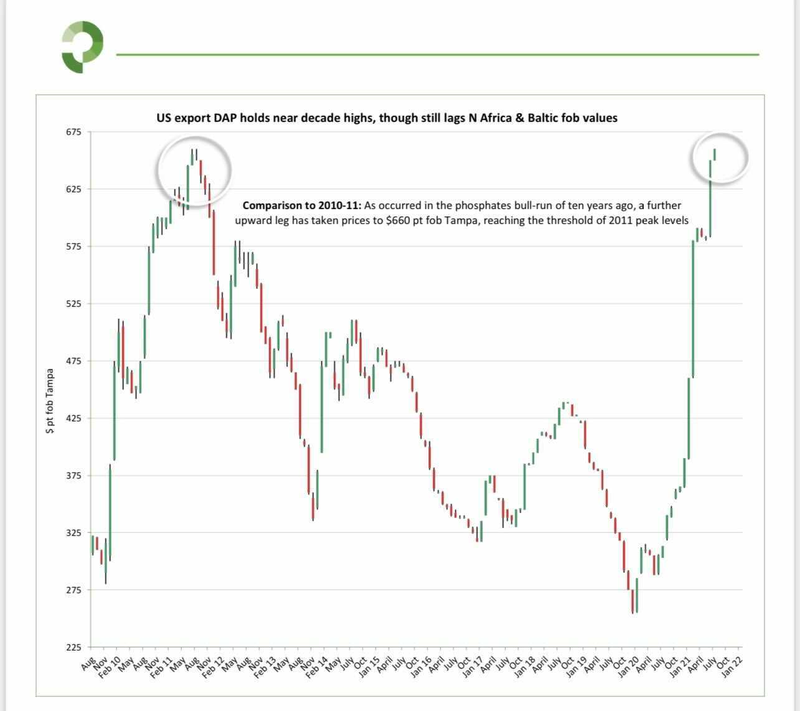

The following World Bank graph provides some context in terms of the extent of the increase in the MAP price, highlighting that it is now trading in the vicinity of a 13-year high, and at levels that have only briefly been exceeded since 2005.

Factors that can support a strong long-term MAP price

There are a few factors to consider both on the supply and demand sides of the equation when determining the degree of sustainability that applies to the MAP price.

Similar to most commodities, a consideration in terms of the supply side should also extend to the potential for cheaper priced alternative products to enter the market.

With regard to MAP, the competing product requires phosphoric acid production which has a high capital intensity, suggesting it is unlikely that this would emerge as an alternative source of supply.

Given these factors and the general consensus that demand for products that will stimulate food production will only increase in coming years, it could be argued that the market and pricing metrics are more likely going through a period of recalibration to account for an escalation in demand for the nutrients MNB will be producing.

It would appear highly unlikely that the MAP price will decline over time despite the potential for peaks and troughs along the way - with arable land decreasing and the demand for agricultural crops increasing due simply to population growth, the broader outlook supports an uptick in demand.

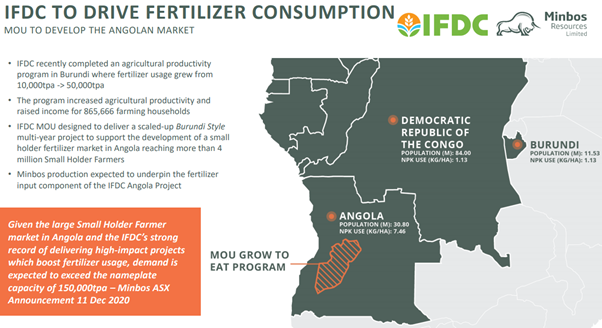

As indicated below, The International Fertilizer Development Center (IFDC), a public international organization working to alleviate global hunger, has completed an agricultural productivity program that resulted in fertiliser usage growing from 10,000 tonnes per annum to more than 50,000 tonnes per annum.

With the IFDC’s involvement in multi-year projects that will support the development of a small holder fertiliser market in Angola that will reach more than 4 million smallholder farmers, fertiliser usage and demand is expected to accelerate to a point where it will exceed MNB’s nameplate capacity of 150,000 tonnes per annum.

The emergence of new supply when it eventually does occur would not be an overnight factor as the underlying mineral resource isn’t readily available, and as has been the case for MNB, regulatory issues, the completion of studies, offtake agreements and financing all takes time.

Identifying peer comparisons

When attributing valuations to the likes of mining projects, the number-crunching we have undertaken is usually central to the process.

However, peer comparisons are another means of gauging fair value.

This is relatively easy with the likes of precious and base metal stocks where there are numerous projects to choose from that have relatively close like-for-like attributes.

By contrast, MNB is operating in a fairly niche area and we wanted to identify an ASX-listed company that was valued at around the $100 million mark relative to market capitalisation, while also being at a similar stage of developing a project that was aimed at producing a commodity for the agricultural industry.

Australian Potash Ltd (ASX:APC) which has a market capitalisation of about $80 million is in the process of developing the Lake Wells Sulphide of Potash Project in Western Australia.

The end product will have applications in organic farming.

Studies conducted by APC suggest the group will be at the plant commissioning stage towards the end of 2023.

Analysts at Shaw and Partners initiated coverage of the stock in April, and their forecasts point to maiden production commencing in fiscal 2024, moving to full production in 2025.

The broker forecasts that the project will generate EBITDA of $74 million in 2025, increasing to $83 million in 2030.

Shaws has a share price target of 32 cents on APC, implying an enterprise value of approximately of ~$220M at an EBITDA multiple of 2.64.

By comparison, scoping study projections point to MNB generating EBITDA of approximately A$120 million in 2030 based on a MAP price of US$643 per tonne, which allows for an 18% fall in the MAP price.

Should MNB trade on a like-for-like EBITDA multiple, its implied enterprise value would be $317 million, representing a share price of roughly 63.8c.

APC’s pre-tax NPV is A$415 million, well shy of the MNB Project’s NPV of A$540 million based on a MAP price of about US$643 per tonne (remember, current price is US$780/t), once again suggesting that MNB’s share price by virtue of the implied project value should reflect a substantial premium to that inferred by Shaws’ price target.

Remember that these are just our rough calculations AND there is a lot of work to be done before MNB gets into production, and also the geographical location in Angola will likely add a risk factor discount compared to WA.

Peer Comparison - Costs are the clincher

MNB’s metrics become even more compelling when you consider APC’s upfront costs, costs of production and the substantial debt funding required to get the project off the ground.

The capital costs to get the Lake Wells Project up and running are $266 million should management’s contingency of $26 million not be required.

As previously mentioned, taking into account increased steel costs the upfront capex for the MNB Project is forecast to be in the vicinity of US$35 million (assuming increased steel costs), representing about $46 million in Australian dollar terms.

APC estimates it will require debt funding of about $185 million to build the project, suggesting it may well be tapping shareholders to fill the circa $80 million shortfall - the group had cash of $14.3 million as at 31 March 2021.

While MNB isn’t sitting on a big enough cash pile to fully build out their project, the fact that the project is much more economical to build, suggests that the need to raise capital by share placements should be more constrained.

The level of debt funding (should that be an option) will also be more modest, resulting in more moderate financing costs.

These factors are reflected in the internal rate of return (IRR) with the APC project having an IRR of approximately 20% compared with the MNB Project’s 66% based on the 18% discounted MAP price of US$643 per tonne.

Consequently, it doesn’t matter which way you look at MNB, whether it be financial metrics, industry dynamics or peer comparisons, we believe it comes up trumps and is why we are holding a long term position.

With the benefits of a proven management team, the company should be well-positioned to take advantage of its premium project at a time when demand for fertilisers definitely appears to be undergoing a sustainable/accelerating upward trend.

Why we invested in MNB

We first took a long-term position in MNB in August at 3 cents and in February we doubled down after MNB completed an oversubscribed $7.3M cap raise at 8c.

Here’s a reminder of why we first invested and why we are invested for the long term:

- Low Capex required of between US$22-28M

- High After Tax NPV of US$159-260M (from when we first invested a year ago)

- Near term share price catalysts on the horizon

- It’s current low market cap

And here’s a broader overview of why we like MNB:

Market opportunity

Spending on food in Angola is expected to increase from US$15BN in 2017 to US$21BN by 2021, however the country needs assistance to grow crops. Minbos is aggressively targeting first supply of nutrients for Angola in 2021.

World class project

Minbos’s Cabinda Project is a world-class phosphate ore project.

Existing resource

Cabinda has an existing resource of 7Mt@30% P2OS.

Scoping Resource

The successful development of a 21-year mine life operation is anticipated to generate EBITDA in a range between US$747M and US$1.1BN, implying a mid-range after tax internal rate of return of approximately 50%.

Offtake agreement

Minbos anticipates signing an off-take agreement with the Angolan government as part of the DFS before the final investment decision (FID)

We originally invested in MNB because at the time, we thought it was the most undervalued stock in our portfolio when it was under $20M market cap.

MNB has progressed since then and is now capped at ~$40M and we think has a long way to go.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.