PUR maiden lithium JORC resource - and drilling hasn’t even started yet…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 51,165,999 PUR shares and the Company’s staff own 950,001 PUR shares at the time of publishing. The Company has been engaged by PUR to share our commentary on the progress of our Investment in PUR over time.

A maiden JORC resource before drilling has even started...

... based on shallow 200m deep historical drill holes and recent geophysical surveys.

Other lithium explorers nearby have been delivering high grade lithium drill results as deep as 500m.

AND Pursuit Minerals (ASX:PUR) will be drilling deeper this quarter, which should make its lithium resource even bigger.

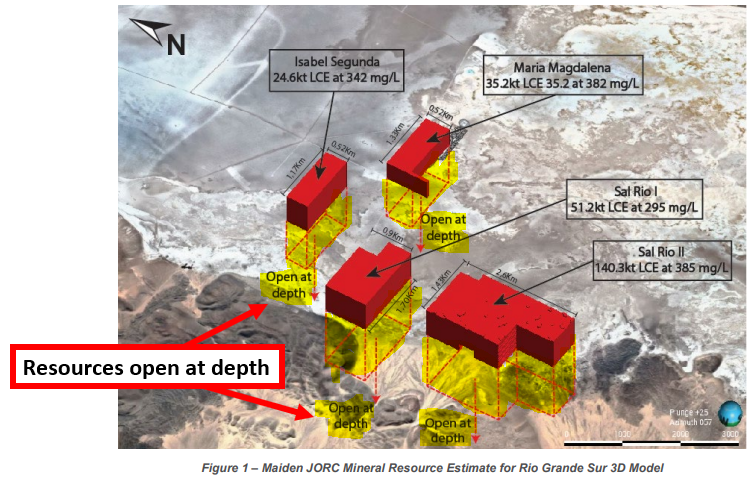

Today PUR announced a maiden JORC resource estimate at its Argentine lithium project inside South America’s ‘lithium triangle’.

Lithium brine projects are a little less understood than their hard rock cousins on the ASX, but they actually hold most of the world’s reserves.

The lithium triangle is home to ~60% of the world's defined lithium reserves and this is where PUR has just managed to define its share of it today.

PUR now has an in ground 251.3kt JORC lithium carbonate equivalent (LCE) inferred resource.

Without poking a single hole into its project, PUR already has a resource bigger than its South American peer $267M Argosy Minerals. Noting however that Argosy’s resource was calculated at a higher level of confidence (indicated) than PUR (inferred).

While an inferred resource is a lower level of confidence in the resource, we expect PUR will be able to eventually move more of the resource into the indicated category with additional drilling.

The added bonus as we highlighted above, is that PUR’s resource is based on historical drilling data down to depths of just ~200m.

AND only covers a fraction of PUR’s ground over the project.

PUR’s ground is yet to see a drillhole deeper than 200m - which means there is scope to increase the size of its resource significantly.

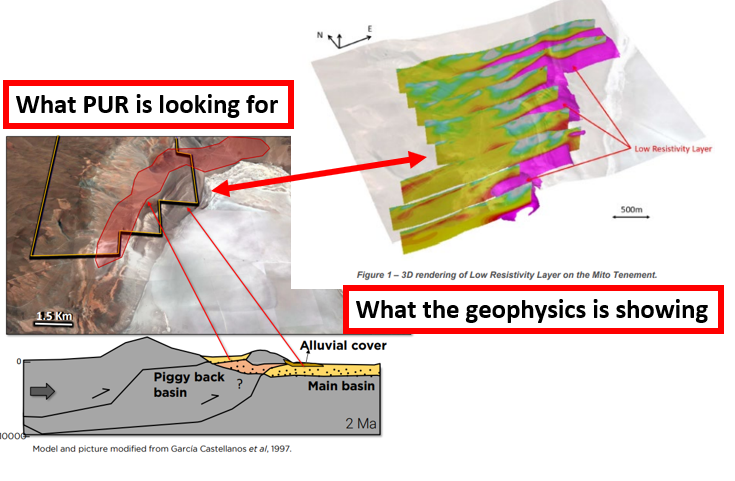

Over the last few months, PUR has been running geophysical surveys showing potential for lithium brines all the way down to 500-600m+ depths.

PUR plans to drill the highest priority areas before the end of the year.

The goal for that drilling is to see if the brine reservoirs extend at depth AND to see if the lithium grades are getting higher as PUR drills deeper.

Higher grades at depth are something we have seen across other salars (a salt flat which can host lithium brine underground) in Argentina.

One example is the Pastos Grande Salar - where PUR’s CEO has previously had experience.

At Pastos Grande, holes drilled down to ~90-180m had average lithium grades of 538 mg/l...

Holes drilled down to ~365-620m depths had average lithium grades of ~641 mg/l.

So, as companies drilled deeper in Pastos Grande, they kept hitting higher grade lithium structures.

Which means more valuable lithium can be extracted from the asset.

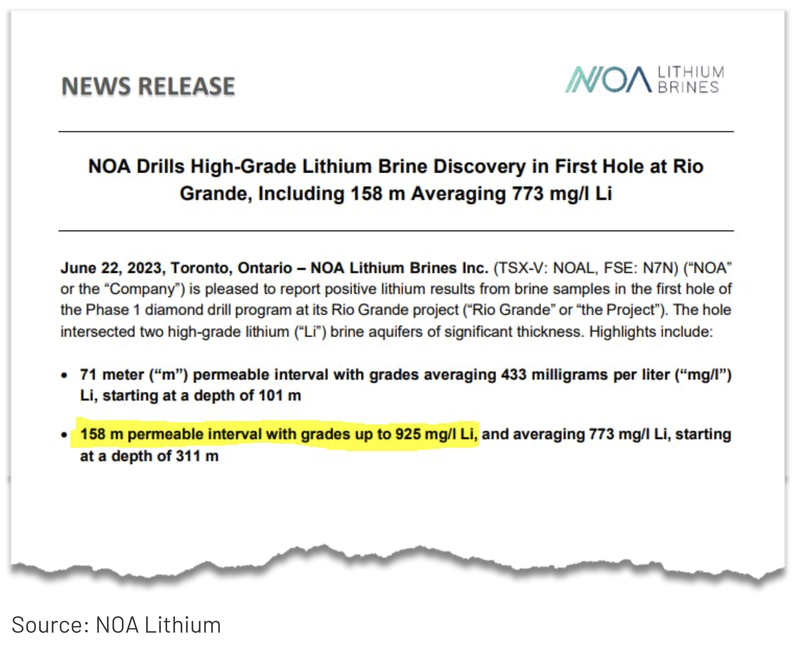

Closer to PUR’s home - one of its peers on its salar, TSX listed NOA Lithium, recently drilled holes to the north of PUR’s ground and was hitting grades of ~433mg/li from depths of ~101m.

Down at depths below 300-400m the grades were increasing to ~773mg/li and ~925mg/li.

(Source)

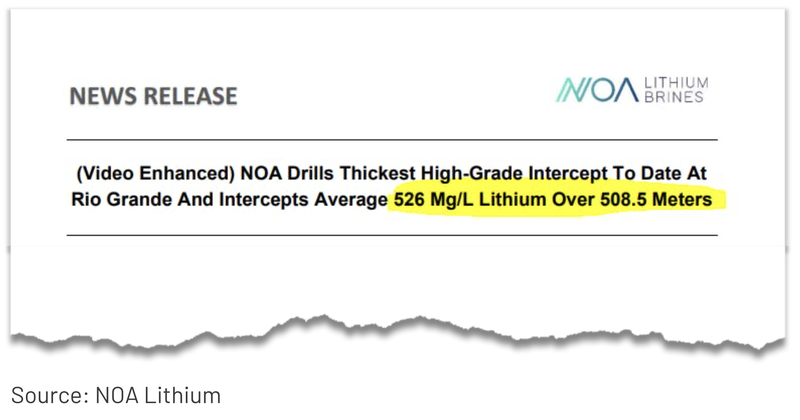

More recently, NOA also hit ~508m intercepts with average grades of ~526mg/li.

(Source)

At the moment PUR’s inferred resource is based on an average grade of 351mg/li...

IF PUR can drill deeper, extend the lithium reservoirs at depth and increase the project's grade then it could quickly multiply the size of its JORC resource...

We think this is the blue sky potential for PUR:

PUR drilling below 200m depths, hitting high grade lithium and multiplying its existing JORC resource.

If PUR can prove both higher grades and extensions, then its JORC resource could start catching up with companies that are capped >10x where PUR is trading today.

Right now PUR is capped at just $26M, whereas its South American peers are capped in the hundreds of millions of dollars.

Today’s maiden inferred JORC resource defines an initial base from which to compare PUR to its peers, but we think that after drilling, the company will start to show the size/scale potential of its project.

We think the Rio Grande Salar (where PUR’s projects sit) has the potential to be one of the biggest and most high grade salars in Argentina. Ultimately this is the kind of outcome we are Invested for.

Once PUR can demonstrate this with additional drilling, we hope the company’s market cap re-rates in line with its peers.

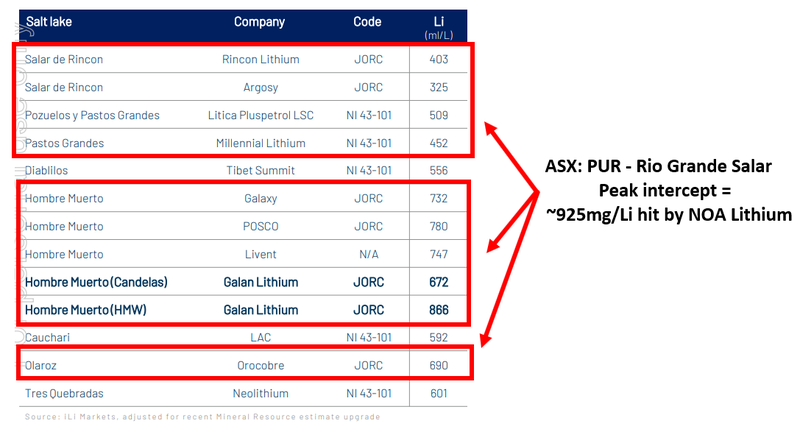

Here is a comparison of Rio Grande with the other Argentinian salars:

(Source)

PUR’s pathway to production

The immediate focus for PUR has always been to define and then increase its JORC resource base.

But in the background, PUR has also been busy looking ahead to production.

Earlier in the year, PUR purchased a processing plant with a replacement cost of ~US$3.6M for just US$360k.

Over the last few months, it's been preparing the plant to start producing battery grade lithium carbonate as quickly as possible AFTER PUR’s drill programs.

PUR has one pumping well planned in its upcoming exploration program, which means we could start to see it take lithium brines from its project and produce battery grade samples not long after.

These samples will allow PUR to operate its processing plant and start tweaking its lithium carbonate product well in advance of any scale up of the project.

This enables PUR to put together battery grade products for product qualification with potential offtake partners/buyers - and tweak the products accordingly.

That makes the whole scale up process a lot easier, with the only constraint then being the cash to build a bigger plant.

PUR’s plan is to get to 2,000tpa production within 24 months and then 20,000tpa within 36-48 months.

Ultimately, we are Invested in PUR to see it do define a large lithium resource and get it into production which forms the basis for our Big Bet:

Our PUR ‘Big Bet’

“PUR increases the size and scale of its lithium project to a level that warrants putting it into production. We are hoping this re-rates the company to a market cap of >$1bn (similar to what peer company Argosy achieved)”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PUR Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

More on PUR’s upcoming drilling plan:

Back in June, PUR outlined its drill programs as follows:

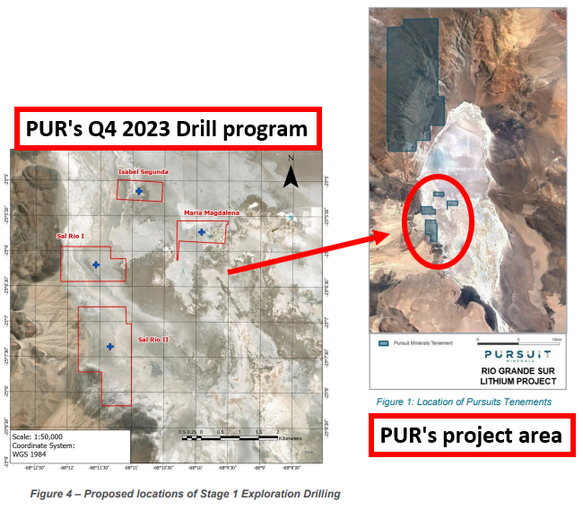

1) Drilling before the end of this year (Q3-Q4 2023)

PUR plans to drill four holes on its ground, sitting directly on the Salar.

This is where the existing JORC resource estimate has been built from.

The existing JORC was done off the back of data down to 200m depths, the drill program will be looking to drill down to bigger depths >500m.

After the four holes are drilled, PUR is planning to drill ONE pumping well to determine flow rates for the project.

Below are the drillhole locations for the first phase of drilling:

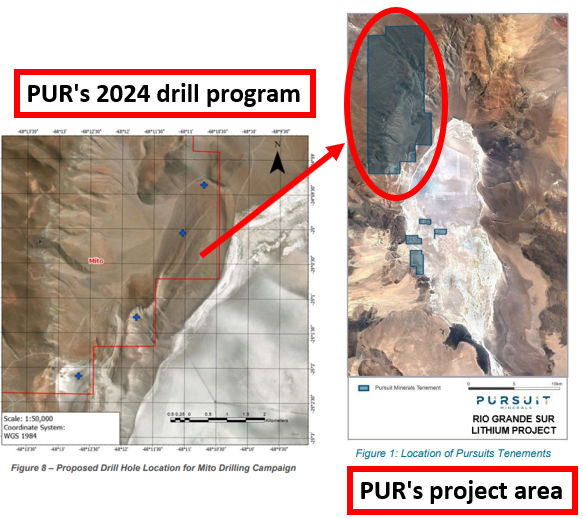

2) Drilling program in 2024

PUR’s next round of drilling will focus on the much larger Mito tenement.

Mito is PUR’s biggest landholding and sits right on the margins of the Salar.

For further context, the significant size of the Mito tenement can be seen below (top left blue square):

Here PUR will be testing to see if the brine reservoirs inside the Salar extend out onto the margins - a theory that PUR’s neighbour NOA Lithium has been testing and successfully proving.

What’s next for PUR?

Drill program (Q4 2023) 🔄

PUR’s plans to drill four exploration drillholes and one pumping well as part of its first drill program.

In today’s update, PUR confirmed that the drill permits were expected to be granted relatively soon, and the drill program is expected to start in Q4 of this year.

Pilot plant commissioning 🔄

In a recent update, PUR also confirmed that its processing plant was relocated to a new facility where commissioning works had started.

Once fully assembled PUR expects to be producing both battery and technical grade Lithium Carbonate - which it can send off to potential buyers/offtake partners.

Interestingly, PUR mentioned that the company had already received “several expressions of interest for the development of the project inclusive of off-take agreements”.

We are hoping the pilot plant is ready to produce lithium carbonates from the brines that might come from the Q4 drill program, before an eventual scale up in 2024.

(Source)

What are the risks?

Now that PUR has defined its own JORC resource, the key risk for the company is around “commercialisation”.

PUR is looking to produce battery-grade lithium carbonate from its pilot processing plant.

There is always a risk that PUR experiences technical issues trying to get the plant back online.

You can see more on the key risks in our Investment Memo.

Our PUR Investment Memo

Along with the key risks, our PUR Investment Memo provides a short, high-level summary of our reasons for Investing.

The Investment Memo details:

- Our PUR Big Bet

- Why we Invested in PUR

- Key objectives we want to see PUR achieve

- What are the key risks to our Investment thesis are

- Our Investment plan

Helpful links to understand this article:

🎓The different types of lithium projects explained

🎓What is a JORC resource? How does a company define a resource?

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.