Two Pronged ASX Developer Attacking Future Proof Lithium and Potash Markets

Published 17-MAY-2017 09:27 A.M.

|

16 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Next Mining Boom presents this information for the use of readers in their decision to engage with this product. Please be aware that this is a very high risk product. We stress that this article should only be used as one part of this decision making process. You need to fully inform yourself of all factors and information relating to this product before engaging with it.

Unless you’ve been hiding under a rock for the past two years, you will no doubt have heard about the upswing in demand for lithium.

In terms of valuations amongst lithium explorers, lithium prices and final end-users of lithium — all aspects of the lithium supply chain have experienced significant growth.

Today’s ASX-listed company has a JORC Resource on track for formal delivery very soon at its lithium project in San Jose, Spain as it looks to enter into the European lithium supply race.

Having a historical (1991) feasibility study on lithium carbonate production on site has given real impetus to the updating of technical studies by this $35 million capped company.

Working in this company’s favour is that the European lithium market has no internal suppliers.

This opens the market up for a savvy, well-funded near-term producer working in a very mining friendly Spanish jurisdiction.

What could also pique investor interest is this company’s close-knit relationship with a big-hitting billion-dollar construction company and mining aspirant, the IBEX 35 listed $1.1 billion capped Sacyr.

The ‘billion-dollar Sacyr’ was responsible for widening the Panama Canal last year, as well as construction of the desalination plant in Perth, WA.

So these are bona-fide specialists with extensive infrastructure-building credentials and insight into global geo-politics – and they have paired up with our $35M capped ASX listed stock.

It must be noted though that like many early stage mining plays, today’s stock should still be considered a speculative investment and investors should seek professional financial advice if considering it for the portfolio.

In terms of project progress, this company has over 10,000 metres of drilling data at its disposal, with the last tranche of 2,000 metres having been completed just weeks ago.

This was part of the confirmation work required to bring pre-JORC resource work into the ASX reporting sphere.

Despite not having any Indicated or Inferred lithium Resources just yet, (these are expected to be ushered very shortly – within weeks) the peripheral data available so far – including a Banco Espagna report from 1993 — shows this company is aiming for a substantial lithium Resource.

This could be the next catalyst for the company and enable it to be compared with its higher valued peers.

Furthermore an exploration target could significantly expand on the historic estimate of 1.15Mt contained Lithium Carbonate Equivalent (LCE) sourced originally from 83Mt @ 0.6% Li 2 O.

These factors combined could lead to a considerable accumulation of metal – one of the largest in Europe.

Once completed, this ASX stock will be able to publish a JORC Resource to the market, and therefore, move its flagship lithium project up the value chain.

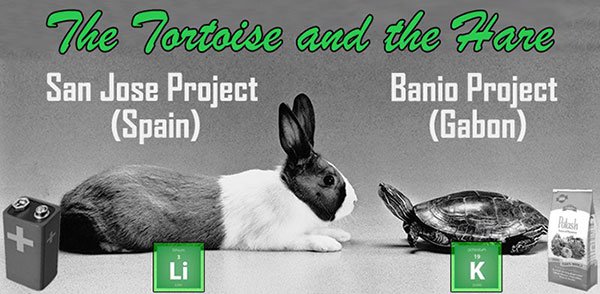

While European lithium is its flagship play, this company is also pursuing another high value, future proof commodity with its potash project in Gabon.

Drilling is currently underway at this project, with historical drilling and seismic already supporting a world class JORC Exploration target. The company’s drilling programme is dedicated to confirming this potential.

Together, these two projects have the potential of placing this company into the diversification sweet-spot, and ensuring it generates strong commercial performance on all horizons. In other words, having a balanced blend of tortoise and hare on its running team.

Unveiling:

![]()

Currently capped at $35M, and with $5.3M in cash on hand at the end of last quarter, Plymouth Minerals (ASX: PLH) is a company intent on stamping its authority in the lithium market. Having cast its line into this rather ‘nouveau’ market back in 2011, PLH has been patiently biding its time, surveying the lay of the lithium land for over 6 years.

It was only in 2015/2016 that lithium made its debut onto the world stage (and into investor portfolios), on the back of the realisation that lithium could potentially become the most highly consumed commodity after crude oil. Goldman Sachs even called lithium “the new gasoline” last year.

The Next Mining Boom has been covering a number of lithium stocks over the past few years which have fared well.

When looking at PLH, one other company springs to mind – European Metals (ASX: EMH). We first alerted our readers to the EMH story about EMH back in April 2015 in the article Electric Cars Need This: ASX Junior’s Billion Tonne Potential .

Since our first article was released, EMH’s share price has gone up over 17 times; as high as 1,700%:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Given PLH is quickly progressing with another highly advanced European lithium project – it begs the question:

Can PLH perform similarly over the coming weeks and months?

But before we delve into the key macro factors likely to support PLH in its mission to find commercial traction over the coming years — let’s go through PLH’s arsenal...

PLH has two flagship projects, in two very different industries.

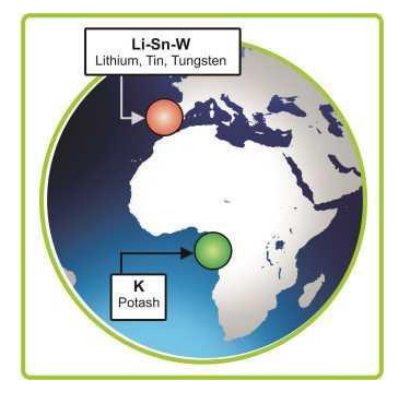

Lithium in Spain — The San Jose Lithium Project

The San Jose Lithium Project is located in Western Spain, close to the Portuguese border. The region is historically known to contain a variety of metals, and was worked on extensively in the early part of the 20th century. Also notice the consistent smattering of existing infrastructure and export-conducive facilities dotted all over Spain – this is a first world country with first world infrastructure and a highly educated work force.

Only very recently however, in the early 1990s, was lithium discovered at San Jose, by Spanish company Tolsa.

A feasibility study completed in 1991 defined an open pit mining operation and a process flow sheet which produced lithium carbonate.

The deposit is unique due to its extensive strike, width and surface outcrop that make it highly amenable to bulk, open-pit style mining methods.

Lithium mineralisation extends from surface to in excess of 300 metres vertically and in excess of 500 metres along strike.

PLH has snuck in and assimilated all the previous data, already done by Tolsa, and is building on this knowledge base to fast track the development of the deposit.

And why wouldn’t they?

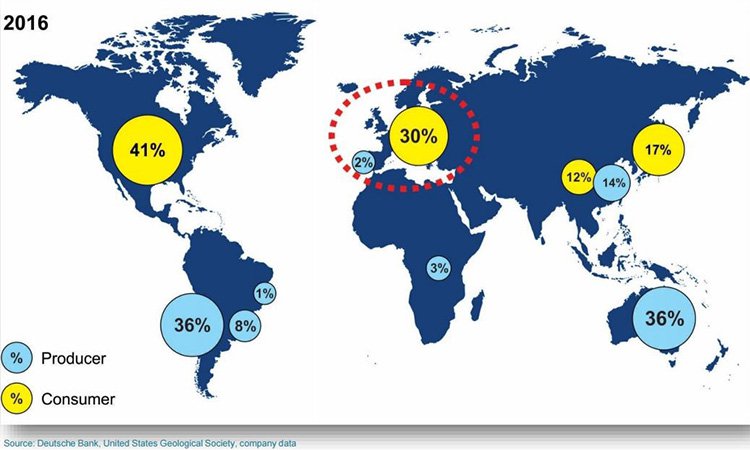

It is a fact that European lithium demand has no effective internal suppliers:

At a minimum, this creates a level of demand certainty for aspiring lithium producers like PLH, and the bullish lithium analyst would call this a burgeoning market to sell into, given the build-up of battery gigafactories anticipated for the European continent.

What could set PLH apart from its peers is that it will extract its lithium using conventional process technology to produce battery grade lithium carbonate on site.

PLH aims to exploit the resource via open-pit mining and this is driven by the extensive dimensions of the deposit and its outcropping nature.

With mineralisation from surface, initial years of mining would be moving just ore.

PLH drilled a program of 10 holes (2 RC and 8 Diamond) for approximately 2,000m at the end of 2016 and in the first quarter of 2017. The drilling was designed to twin historical holes in order to provide maximum support for JORC resource calculations.

The drilling and assay database for San Jose now comprises in excess of 52 holes for 10,000m of drilling including 3,500m of diamond drilling.

Very importantly, PLH’s potential deposit is open at depth and along strike.

San Jose is a highly-prospective project with potential for high-grade zones with a reported Historical Foreign Estimation of Mineralisation of 14Mt @ 0.9% Li 2 O for 133kt contained lithium oxide (Li 2 O) at 0.75% Li 2 O cut off. This is hosted within a much larger global estimate of 468kt contained lithium oxide or 1.15Mt lithium carbonate equivalent.

A selection of significant intercepts from drilling at the deposit demonstrates the wide intercepts that characterise the mineralisation. Intercepts include;

- 45m @ 1.0% Li 2 O from surface hole MSJ-DD-0006

- 250m @ 1.0% Li 2 O from surface hole MSJ-DD-0003

- 142m @ 1.2% Li 2 O from 67m SJ-4C

- 52m @ 1.1% Li 2 O from 18m MSJ-DD-0004

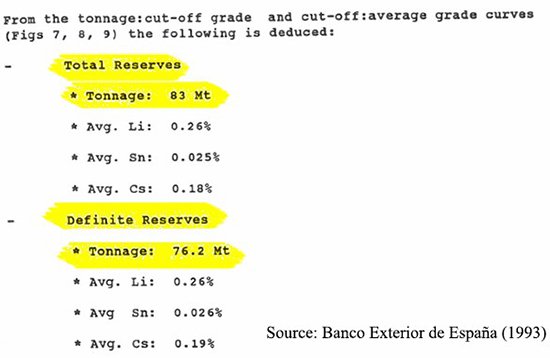

An alternative estimate done in 1993 by Spanish bank BEX, indicates around 76-83Mt of lithium hard rock being available, at an average lithium grade of 0.26% Li.

BEX’s 1993 study came up with a Resource of 83Mt @ 0.26% Li, a 1:1 strip ratio open pit for 13.8Mt @ 0.96% Li 2 O and positive IRR.

The only reason this project did not go ahead back in the 1990s, was because it was not yet lithium’s time, and there was a recession across many other commodity markets.

The developers walked away and left San Jose, teeming with opportunity at some future point in time...

The crucial goal for PLH is to build upon this historical data and their inferences — and quite possibly — expand upon it significantly by using cutting-edge exploration methods, and, welcoming a big hitter to the table.

The big hitters in PLH’s corner are Sacyr and Reabold

Progressing mining projects into commercial territory is tricky and requires plentiful amounts of expertise and funding.

PLH has partnered with ‘goliath-esque’ Spanish company Sacyr, and its wholly owned subsidiary Valoriza Mineria, to progress San Jose in exchange for 25% of the Project’s eventual bounty.

Yet, what comes of this partnership remains to be seen and investors should therefore take all publicly available information into account before making an investment decision.

Sacyr is a construction company worth €1 billion (AU$1.4BN) and with more than €26 billion in current projects that specialises in completing high-profile development projects, such as the Panama Canal expansion done last year. The expansion was hailed as ‘the largest engineering project of the 21 st Century’.

Sacyr are plugged directly into potentially very profitable geo-political entanglements — the fact that Sacyr was tasked with the Panama Canal expansion, and not a peer rival such as Bechtel or Halliburton, suggests that PLH has teamed up with the perfect goliath, with which to progress its lithium intentions.

PLH is required to deliver a Feasibility Study over the next 4 years in order to make good on the deal.

And as we said earlier, PLH is now fully-focused on getting San Jose re-JORC’d in line with the latest estimates.

The other partner in PLH’s corner is Reabold

Sacyr is assisting with technical expertise, while Reabold is all about helping PLH with its financial position, capital raising efforts and global expansion.

What PLH and Reabold want to do, is to raise awareness of PLH’s San Jose Project in several regions simultaneously. Reabold recently listed on AIM market in the UK, and has taken a 2% stake in PLH.

Here at The Next Mining Boom , anytime we see institutional names, both in Australia and overseas, piling into a stock — we tend to pull on our small-cap investor caps and ask the question, why?

Given PLH’s existing partnerships and its overall market activities, we think there’s a reasonable chance for PLH’s dual-pronged commodity race, to be spun off into separate entities for better market traction.

We’ll definitely be keeping a close eye on Reabold, Sacyr and PLH, over the coming weeks because this sprawling corporate enchilada is only just getting started.

The Lithium Story is all about energy, efficiency and long-term energy security for all

Tesla’s highly-anticipated launch of its brand-new Model 3 last year, has got the world buzzing.

Tesla is driving towards an entirely different energy future that is built on better energy storage. The Tesla effect has the potential to shift how the world thinks about energy and, therefore, could affect the values of key raw materials required for an energy-efficient future.

The following article gives a more in-depth look at the evolution of this market:

The ultimate point to make regarding batteries, energy and Tesla is...

...this is only the start.

Can you imagine the rate of lithium demand as and when Chinese and German manufacturers pick up Tesla’s baton and begin to manufacturing products of their own?

It could mean lithium literally becomes the new oil – the lifeblood of tomorrow’s global economy that will undoubtedly reach a point where EV cars outnumber their combustion cousins.

It’s also quite possible that within 50 years, there are no combustion cars left on the road whatsoever, while energy grids could become a lot more redundant than anyone ever imagined.

The technologies entering today’s markets are literally threatening to terraform everything in sight — and much of it is dependent on lithium.

Therefore, we think PLH’s decision to accelerate progress at its wholly-owned lithium project is a demonstration of good common sense, and opportunistic timing.

PLH has waited patiently for over 5 years for lithium to mature as an investable commodity and for end-users such as Tesla to hatch gargantuan world domination plans.

These plans require millions of lithium-stuffed electric vehicles, cutting edge battery-powered power generators and possibly most importantly plenty of paying consumers with fistfuls of dollars.

And, with that, PLH promptly pounced on the San Jose lithium project.

That’s not all folks

This company’s other prong, with which to raise its valuation, is potash.

Potash exploration bears a few similarities to lithium exploration, and with just as much demand-side lustre.

Whereas lithium is going hand-over-fist into batteries and electronic gadgets...

...potash is all about helping to feed the world, which means it is being earmarked as a supplement for farming activities.

Let’s dive straight into PLH’s potash endowment, to see how this commodity can help our small-cap steed

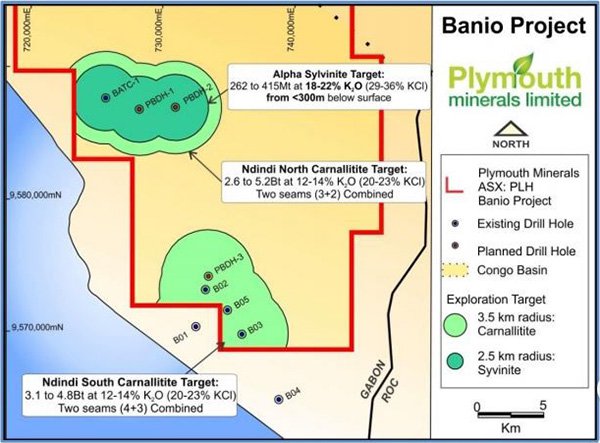

PLH’s Banio Project is located in Gabon.

The Banio project represents an opportunity to bag a multibillion tonne target, already supported by drilling and seismic data.

At the same time, given PLH is operating in Africa on this project, this is a very high risk stock for political and social reasons. Getting mining projects up and running in countries such as Gabon is no simple feat, and there may be challenges ahead.

One only needs to look at companies like Kore Potash Ltd (ASX: K2P), currently capped at $130M who is progressing with its African potash project, to see the pathway to value for the $35M capped PLH.

The Banio Project covers 1,244km 2 and is centred 450km to the south of Libreville along the Atlantic Coast.

PLH wants to convert historical exploration and the current Target Resource into a fully-fledged JORC Resource that can be used to attract further funding and potential offtake agreements.

Possibly the sharpest edge to PLH’s potash ambitions, is the potential to produce low-cost potash that is inclusive of transport costs for buyers.

Currently, when potash is priced for customers, it is billed without including the cost of transport. When these costs are later added, the actual cost of potash for delivery can be rather higher than the headline price.

PLH thinks it can substantially undercut other potash producers, even those much larger than PLH, by producing a more transparently-priced product which is only possible in low-cost regions such as Gabon.

To give you a ball-park estimate of the tonnage that PLH could have access to, PLH’s Banio project is 20km away from Sintoukola which is reported to contain a global resource of 5.3 billion tonnes of potash mineralisation at 14.3% K2O (22.6% KCl) .

Based on 2D-seismic interpretation and information from 6 historic drill holes which intersected potash, industry specialist consultants CSA Global have since delineated a significant Exploration Target.

The Exploration Targets are in two areas and cover a combined area of 126km 2 within a larger area that is also prospective for potash mineralisation.

Potty about Potash

The market for soil fertilizers including potash has been climbing steadily for decades. The globe is forecast to have over 9 billion people by 2050 which is already putting a huge strain on food production around the globe.

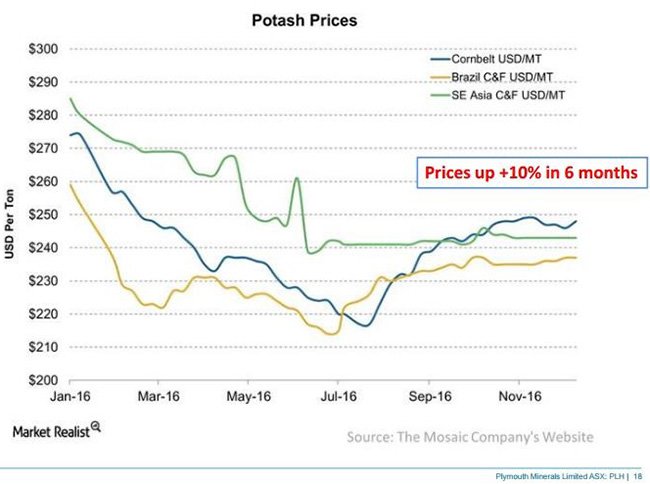

Here’s a look at the price trend for potash to November last year.

As you can see, demand and price are once again trending upwards.

The other challenge for farmers is that attempting to achieve better yields through more intensive farming methods, eventually leads to soil degradation and lower yields over time.

The amount of land available for farming (arable land) has therefore been falling since the 1960s. In many ways, fertilizers bridge the gap between what a farmer can grow and what he wants to grow. In fact, use of fertilizers is now so widespread, that over 30% of all produce is now grown with their assistance.

The business of agribusiness

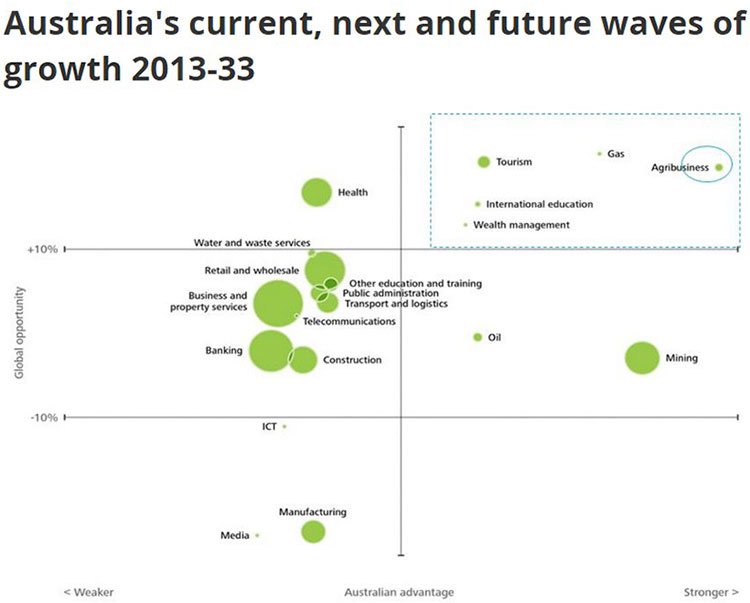

If we look at the market for agribusiness in Australia, it too indicates fertile ground for the foreseeable future, much like lithium. The business of agribusiness is to grow more crops, from less space — this requires a heap of potash (fertiliser).

A scatter plot shown below, forecasts growth for various Australian sectors going into 2033, published by Deloitte.

PLH is in prime position because its run-up to production is expected to take around 1-2 years.

Here at The Next Mining Boom , we think PLH is on the right track to become an economically-viable potash player, backed by tectonic industry shifts, low-cost mining and a global food-security elephant that refuses to leave the room.

Companies like PLH can step in and secure an operational advantage — therefore becoming a best-of-breed producer, at just the right time.

Greater than the sum of its parts, and with both a Hare and a Tortoise on its books

We see PLH as a timely pick-n-mix opportunity, in today’s uncertain commodities markets.

The world is right in the middle of a shift from traditional power generation (and storage), to a much better alternative. This new-age transition is being felt in other industries too, such as potash.

PLH is making a short-term bid for lithium — with a JORC Resource at San Jose, very likely to be winging its way to PLH’s inbox later this year.

What the lithium market underlines, is that this commodity is here to stay for generations. Future EVs, gadgets and energy storage solutions will all have substantial amounts of lithium woven into them – and it won’t just be Tesla hogging all the supply.

Come to think of it, PLH and lithium have something in common —both are progressing fast, both seem on the cusp (or undergoing) significant re-ratings, and both offer investors neat exposure to the new energy universe we seem to be careering into.

With two projects at the starting gate, but offering very diverse market opportunities, PLH is looking for project development finishing lines already on the horizon.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.