Is China’s Graphite Dominance Walking the Plank?

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The production capacity of lithium-ion batteries is set to more than triple by 2020.

LG Chem, Tesla, Foxconn are just some of the big companies looking to build factories to meet the flood of demand anticipated for lithium-ion batteries.

Regular readers should be well aware of graphite’s part in the equation – it’s a key component of lithium ion batteries, and more specifically within the anodes of the batteries.

But not just any kind of graphite can be used in lithium ion batteries. What is required is “ultra-pure graphite” – which is either:

- Synthetic and costly to produce from natural, large flake graphite, or;

- It’s naturally occurring – as ultra-pure fine flake graphite.

Typically, graphite producers will deliver 90%-95% TGC to be upgraded to a higher grade artificially by third party processors – adding to their production costs and cutting their margins.

But that does not seem to be the case for our latest company:

This ASX explorer has found a way to produce battery grade graphite without the need for jumbo flake sizes or expensive processing methods to produce synthetic graphite.

This company expects to produce graphite with Total Graphite Content (TGC) greater than 99 % – obtaining the best market prices.

The added bonus is that this explorer’s operations and future production will be done from Australia – with top-notch infrastructure and an ultra-secure operating climate.

China currently supplies about 75% of the graphite market, and have pretty much sewn up most of the emerging African production capacity of graphite via offtake agreements.

Now other nations like Germany and the US want their own slice of the market, and they may turn to this ASX company as the right offtake partner for them...

This explorer has sole access to Australia’s largest JORC graphite resource – 8.55 Mt @ 9.0 Cg, for 770,800 tonnes of contained graphite.

The company has the ability to produce high TGC graphite from small flake size that should be suitable for all top-end applications, including the manufacture of graphene. It’s aiming for at least 10,000 tonnes per annum of battery grade graphite production.

Best of all, the company is expecting to go into production as early as next year, but only has an $8M market cap...

At the same time, this ASX explorer is a speculative stock, and caution should be applied before considering as an investment.

A near term catalyst for this company is likely to be the confirmation of an offtake partner for its graphite – the company is currently in discussions with potential graphite buyers from across the world, and test samples are being examined by potential suitors...

It’s not only graphite that this company has its hands on – it also owns the world’s largest cryptocrystalline magnesite resource – this could be divested in the near term, potentially providing a large, near term capital injection into the company...

Introducing:

![]()

Archer Exploration Ltd (ASX:AXE) is a minerals explorer with a series of prospects dotted across South Australia and is currently advancing projects with various metals and minerals including copper, gold, magnesite, manganese and its top focus, graphite.

Mining is only a small part of AXE’s graphite business because the company’s true value-add comes not from obtaining huge quantities of a particular kind of graphite, but rather from extracting a variety of graphite types and manufacturing premium grade graphite in-house, without the need for a third-party to upgrade its finished product.

As well as its rapidly progressing graphite projects, the company also owns the world’s largest crypto crystalline magnesite resource at Leigh Creek in South Australia , totalling 453 million tonnes with a grade of 41.3% MgO – this is almost 50% of the world’s total resource of this type of magnesite...

If you don’t know what magnetise is, don’t worry, neither did we – but on further inspection this is a very important mineral with diverse applications – the mineral is used to make Magnesium and as well as caustic calcite magnesia (CCM). CCM is used to neutralise acids, purify water, land remediation and in feed lots for farming purposes. Raw magnesite is used for surface coatings, landscaping, ceramics and as a fire retardant.

Ultimately, AXE are looking to sell their magnesite asset in the near term – which would generate an immediate cash injection to the company and allow them to expedite their delivery of their flagship graphite projects.

And with the recent shutdown of Alinta Energy’s coal mine at Leigh Creek, the South Australian government needs to generate jobs in the region, and fast – could this help spur AXE’s magnetise asset along?

The discussions on the sale of this asset are going along in the background for AXE, so for the rest of the article, we will be focussing on their graphite projects, which hold the most potential for this company for long term growth from its current sub $10M market cap.

AXE’s Graphite Trinity

In total, AXE has 2,154 km 2 of land under tenure on the Eyre Peninsula in South Australia with 3 graphite deposits and 10 prospects identified to date. AXE’s three advanced graphite projects are shown on the map below:

AXE has effectively found a sweet spot whereby it can tap an abundant supply of varied graphite types as well as produce a high-end product with high market value. Each of AXE’s three advanced graphite projects are 100% owned, and essentially allow production of three different graphite types, supplying three different markets:

- Campoona Shaft: This is the most advanced project of all, with a JORC resource of 1.65Mt at 9.1% GC for 151,400 tonnes of graphite. This site can produce ultra-pure graphite, with strong project economics.

Campoona Shaft had a draft mining lease submitted in May this year, and the overall aim is to achieve open-pit mining of 140,000 tonnes of graphite ore and at least 10,500 tonnes of battery-grade graphite per year. As high-grade graphite can often fetch a significant premium, Campoona Shaft has potential to be a +$200M sized operation and this doesn’t even include Campoona Central which is undergoing further testing (a further 0.52Mt at 11.2% GC for an additional 58,000 tonnes of graphite). Success with Campoona Central testing may extend Campoona mine life by a further 5 years.

- Sugarloaf: Early test work has shown that this project has potential to produce bulk graphite, for end use in fertilizers, and has an exploration target of 40-70Mt @ 10-12% TGC.

- Wilclo South: This is a large flake JORC resource of 6.38Mt @ 8.8% Cg (5% Cg cut-off) and a potential mine life of 20 years of flake graphite.

Considering that graphite can sell for between $1,000 – $30,000 per tonne depending on the quality, the future commercial potential that AXE have on their hands is significant.

The company is actively courting offtake partners for its graphite, and we are looking out for any news on this front soon...

AXE could become one of the world’s only boutique graphite producers given their ability to source varied types of graphite, and produce ultra-high quality products all from the same project site. The final product can be specialised and brought up to whatever standard required by the end user – we will get to AXE’s processing abilities shortly.

And it’s all going to be done from South Australia, a safe jurisdiction with good infrastructure that is well positioned from end-user markets such as China and other surging Asian economies.

In the next section, let’s get acquainted with all the latest on graphite, and the market AXE are set to enter.

Our Track Record

Did you see the Next Tech Stock article on Crowd Mobile (ASX:CM8) New ASX Tech Company has the Answer? Since this article was released, CM8 has climbed as high as 85%:

Source: Etrade

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The Graphite Bandwagon is Underway

Over the past 10 years, graphite has flown in like a bat out of hell into the consciousness of mining investors the world over.

Graphite, as well as being used in lithium-ion batteries, is used to make graphene – a substance one atom thick, and 200 times stronger than steel. The rate of patent applications for graphene, highlights how much excitement and momentum this material currently has:

Total number of published graphene patents by publication year, Source: IPO

With so many patents being published, graphite (and its derivative graphene) is expected to be used in dozens of appliances and products such as electric cars, laptops, mobile phones, batteries and flat screen TV’s.

Even Today Tonight Adelaide has covered graphene and its futuristic applications – to learn more about South Australia’s graphite industry you can watch the clip here :

With so much hype and expectation surrounding graphene, explorers are scrambling over themselves to get their hands on significant commercial graphite resources – and AXE is one such explorer leading the charge in Australia.

The sheer number of patents points the way, but regardless of the futuristic and novel uses of graphene, the rise of graphite demand is driven largely by electric vehicles – here you can see the predicted growth in graphite demand over the coming decades, with Electric Vehicle (EV) demand in blue:

So what is fairly clear is that the biggest consumer of future graphite production is likely to be battery manufacturers such as ‘Tesla’ and ‘LG Chem’.

But it’s not just batteries for electric cars – the Powerwall was introduced by Tesla CEO Elon Musk as a wall-mounted energy storage unit that can fully power a residential home for under $3,500 – this could be a widespread energy revolution, powered by lithium-ion batteries... no one knows just how far this battery revolution could go.

In a sign of the anticipated pending surge in battery sales, Tesla is building a Gigafactory – a gargantuan 35Gwh structure being built in Nevada to manufacture lithium-ion batteries. This will allow Tesla to deliver on its plans to build at least 500,000 electric cars per year by 2020.

Tesla, LG Chem and another battery makers are looking for jumbo flake sized graphite to use in their lithium-ion battery production but unfortunately for them, the largest flake size is found only in Africa, in places like Mozambique, which appears to have been almost entirely taken out by Chinese buyers.

With 100% owned graphite resources in Australia, AXE have a point of difference in the market, and we would expect downstream buyers located in nations other than China to be very much interested in what AXE can provide.

What really caught our eye with AXE is that the company is not pinning all its hopes on one large graphite resource. AXE is complimenting Australia’s largest JORC resource with technical ability that will facilitate the highest possible grade of graphite at + 99% Total Graphitic Content (TGC) – more on that soon.

But first let’s take a quick look at the influence China has on the graphite market.

Flake Size Doesn’t Mean What it Used To

The largest supplier of graphite in the world today is China.

However, the vast majority of graphite coming from Chinese producers tends to be of the small flake variety which is not best suited for high-end applications such as batteries and graphene.

Small flake graphite tends to be used for industrial applications and tends to fetch a lot less when sold, compared to large/jumbo flake graphite which is used in high margin products such as electric cars and graphene.

For this reason, graphite explorers are obsessed about resource size and flake size. And it’s also the reason why Chinese graphite has limited scope in how it can be applied and what type of finished product it is able to facilitate.

What if there was a company that could produce small flake graphite in large volumes, large flake graphite with high purity AND be able to upgrade all its graphite greater than 99% TGC on demand?

Well, AXE has thrown its hat into the ring as one such company and already, industry experts are taking notice...

Yes, AXE Can

AXE’s processing results of their ultra-pure graphite potentially mean is that flake size is no longer a talking point when exploring for graphite.

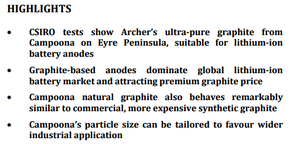

One of the key validators for AXE’s claims is independent verification obtained from the Commonwealth Scientific and Industrial Research Organisation (CSIRO). CSIRO is Australia’s leading multidisciplinary research organisation and is highly regarded in the mining industry.

AXE recently obtained CSIRO confirmation that their smaller-sized graphite flakes CAN be used in lithium batteries and fertilisers:

This was such big news that upon AXE’s announcement on May 7 th that CSIRO had independently verified AXE’s Sugarloaf graphite results, AXE’s stock price jumped 39%:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

And here are the highlights of that CSIRO report:

The key takeaway is that AXE’s graphite can be used in lithium-ion batteries and that AXE can produce natural graphite that is just as effective as its synthetic variant – only much cheaper to produce.

Furthermore, as battery manufacturers keep improving the quality of their products, battery capacities are expected to further improve at “finer micronisation sizes”. AXE is now in the process of commissioning the CSIRO to further test Campoona’s graphite at different particle size distributions to confirm this expectation.

If the CSIRO confirms AXE’s graphite can be produced at ultra-small micronisation, AXE will be able to further improve the quality of its final product and potentially attain even higher sale prices for its graphite tonnage.

Not only have CSIRO validated AXE’s product but as part of a separate existing 2-year $200,000 research program, the University of Adelaide’s School of Chemical Engineering has confirmed that raw, run-of-mine Sugarloaf graphite has naturally elevated levels of macro and micro nutrients and may be suitable for use as a soil conditioner/fertiliser .

According to the report, 9 out of the 13 elements required for plant growth have been found at AXE’s Sugarloaf site which means AXE can divert a portion of its graphite production to the fertiliser industry. By being based in Australia – a huge market for fertiliser products – AXE is conveniently placed close to point of sale.

This additional revenue channel is yet another diversifier for AXE therefore adding to the investment case for this nimble boutique player.

AXE’s Three Graphite Projects in Detail

Now let’s take a detailed look at the three projects that have the most commercial potential for AXE...

Campoona Shaft:

Campoona Shaft used to be an old graphite mine which has been ‘rediscovered’, so to speak. AXE identified this old mine’s potential and is working hard to bring it back into production.

This is AXE’s flagship project, set to produce ultra-pure fine flake graphite at 10,000 tpa with a forecast mine life of 14 years.

As we indicated above, graphite samples from Campoona have been CSIRO tested and independently verified to perform to the same standard (and better) than synthetic graphite.

One of the great advantages for AXE is that the site is open at depth which means future exploration can be extended. So combined with the fact AXE is exploring at shallow depths, future exploration is likely to be cheap, fruitful and extendable if required.

The site has premium infrastructure including nearby reticulated water, high-voltage power and excellent roads. All the components are there for initial production to begin in earnest.

No other Australian company can achieve a 99%+ TGC product, ready for market from within the same site as AXE is able to do. That is a significant competitive advantage that will not only hold AXE shareholders in good stead, but will also send a clear signal to Chinese producers that the Australian mining boom hasn’t gone anywhere.

Sugarloaf

The Sugarloaf site is AXE’s bulk graphite production site earmarked to produce lower flake size graphite for use in the fertiliser industry. According to Adelaide University and AXE’s own detailed research, the Sugarloaf project can produce amorphous graphite with high zinc and potassium content.

This means graphite extracted from this site should be suitable for use in fertiliser products which Australian farmers are keen to buy. Sugarloaf graphite will be a good revenue diversifier for AXE and not only that, will add value to its main revenue driver – high grade Campoona 99%+ TGC graphite that has the potential to sell for over $30,000 per tonne.

The great thing about the Sugarloaf site is that it is next to AXE’s planned Sugarloaf Advanced Graphite Processing Facility. If AXE were to obtain just $10 per tonne for such graphite, the revenue generated could be between $400M and $700M. However at the same time this is very early stage, and there are a few hoops AXE need to jump through and a bit more testing to finish before AXE start earning cash.

Adelaide University have confirmed that AXE’s graphite is suitable for fertiliser products, so as soon as an off-take agreement is sealed, AXE could be raking in supplementary revenue here.

Wilclo South

Last but not least, the Wilclo South project is AXE’s large flake graphite source with a JORC resource of 6.38Mt @ 8.8% Cg (5% Cg cut-off) and a potential mine life of 20 years. The site has proven production of large and fine flake graphite at grades of 91-93% Cg and flake content approximately 50%.

The site could be explored further having had only 20% of its targets drilled, but AXE is prioritising towards other sites to expand its JORC resource.

In total, AXE’s project portfolio has three graphite prospects – two are at an advanced stage of development and one already has a JORC resource – thereby giving AXE a diversified shot at graphite production.

Taking out the Butcher

AXE seems to be blossoming as a future “boutique” graphite producer. The clothing equivalent of a designer label, that’s able to produce high-quality premium priced products with allure, rather than bulk product with low quality.

Typically, graphite producers will deliver 90%-95% TGC graphite to be upgraded to higher-grade artificially by third-party manufacturers which unsurprisingly adds processing, transport and storage costs.

This additional process can be avoided by obtaining 99%+ TGC graphite directly, by intervening in the ‘paddock to plate’ routine and taking out the butcher.

This is exactly what AXE is doing at its Campoona Project.

AXE is able to upgrade its own graphite from the ~95% TGC found below the ground, up to 99%+ TGC after processing. Graphite prices are mostly driven by TGC content, and 99.9% TGC usually fetches in the region of US$30,000 per tonne. Higher grades will fetch even higher sale prices.

Importantly AXE is able to produce a high TGC graphite naturally. This means production costs are kept low while the sale price remains high. As soon as you drop the quality down to 95% TGC, the sale price falls rapidly down to $2,500 per tonne.

Most of the world’s graphite is synthetic and costs in excess of $7,000 to produce – but AXE is able to produce a natural graphite, with high TGC content for around $1,600 per tonne... This is a much better margin for AXE.

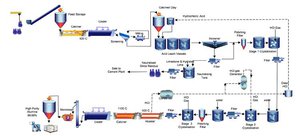

Not only that, but AXE is capable of filling the role of explorer, producer AND manufacturer by completing the whole product chain themselves, as you can see below:

Bear in mind that the graphite market globally is rather small. Approximately 2 million tonnes of graphite is consumed each year with around 50% coming from natural sources and 50% made synthetically.

Given the small size of the current market, if existing producers in Mozambique such as Triton Minerals (ASX:TON) and Syrah Resources (ASX:SYR) come online, the market price is likely to fall.

The potentially lucrative opportunity for AXE is that by focusing on premium high-grade production, AXE can insulate itself from a sudden increase in supply because high TGC graphite is likely to remain difficult to source and maintain a high margin because of a lack of substitutes.

It’s early days for AXE and hard figures have not been released, but let’s assume AXE are able to produce a tonne of 99%+ TGC graphite for approximately $1,000/tonne – this could be sold for over $3,000/tonne at market, which would net a healthy $2,000 margin on each tonne produced...

For an explorer with such strong production estimates, capped at under $10M, the potential is clear.

With that being said, readers of The Next Mining Boom as well as all investors should bear in mind that there is often blue sky potential with many different stocks... But not all stocks fulfil it. Therefore it is imperative for all potential investors to be aware of the risks, not just the potential blue sky rewards.

Looking Forward

AXE is quietly confident that its mining lease will be approved at the start of 2016 enabling the explorer to begin construction of a processing plant in Q1 2016, and be ready for production less than 12 months after that.

AXE will require approximately $36 million to build a 10,000tpa processing plant and in order to fund this, the company is actively talking to offtake partners.

This is a key catalyst for the company, which hopefully shouldn’t pose any kind of issue considering the rapidly expanding use of graphite and its growing demand.

CSIRO and University of Adelaide stamps of approval are also a bright attraction for AXE graphite.

Instead of giving away money to the graphite processors & manufacturers, AXE plans to conduct the graphite upgrading process themselves. By cutting out the butcher, AXE is able to make higher margins and most importantly, target the high-value, premium portion of the graphite market by providing 99%+ TGC graphite.

In China’s Shadow

Despite all the excitement surrounding graphite and graphene, the unfortunate reality is that these markets are currently in China’s shadow.

And there’s a bucket load of political reasons why significantly large companies, namely in the US and Europe, are struggling to do business with Chinese companies.

China currently dominates global graphite production with 80% of all sold graphite coming from Chinese firms. Chinese producers were able to achieve this via binding offtake agreements signed at a rate of knots over the past 10 years.

Due to various political shenanigans, a large proportion of U.S and European markets prefer not to be dependent on China for graphite supply, which is playing into AXE’s hands.

AXE has an abundant source of graphite in a jurisdiction that can bridge the supply gap between East and West.

Another important aspect for AXE, is that the majority of graphite coming out of China is small-sized flake that’s predominantly synthetic.

Synthetic graphite is made by heating up ‘coke’ and carrying out a complicated production process that is often messy and wasteful with the final product costing between $7,000 – $20,000 to produce, as we indicated earlier. Synthetic graphite is a lot more cumbersome to produce than the natural variant both in terms of financial cost and environmental impact.

The potential impact on AXE is that a natural form of graphite suits the renewables energy story much better and is likely to mean manufacturers like ‘Tesla’ and ‘LG Chem’ will prefer to use natural graphite as more of it becomes available.

By operating from Australia, AXE is in a safe jurisdiction and can service the need for a more diversified graphite supply globally. AXE can also undercut the currently high synthetic graphite prices being set by Chinese producers.

It seems like AXE is ‘fighting the good fight’ for a more diversified graphite market with a level playing field for all.

In possession of the largest graphite JORC resource in Australia, AXE is well positioned for a potential Australian mining renaissance driven by graphite.

Taking Stock

In AXE, we think we have found a strong addition to our Next Mining Boom portfolio...

The explorer has an existing JORC graphite resource, is close to entering production and best of all, has several tricks up its sleeve to ensure operational supremacy over its closest peers and rivals.

The main advantages for AXE is that its metallurgical team has crafted a way of supplying what graphite end users want most (high TGC) produced from low sized flake that is most abundant globally as opposed to jumbo flakes.

On top of that but AXE has secured Australia’s largest JORC resource for BOTH Graphite and Magnesite that could see the explorer potentially generating billions of dollars in revenue alongside ever expanding graphite applications... At the same time, its early days for AXE, there is no guarantee they will generate revenue, and this company remains a speculative stock.

Down the track, AXE could evolve to manufacture graphene end-user products, another potential revenue driver as and when the graphene industry settles down and its applications become clear.

All in all, we think AXE is a company that has leveraged itself towards one of the most future-proof minerals currently available and has taken a diversified approach to achieving its ambitions.

If graphite and graphene become as ubiquitous as analysts (and eager consumers) are expecting, AXE could be spearheading Australia’s next mining boom as a boutique graphite producer – with a magnesite kicker to boot.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.