BHP and RIO Unable to Compete: Upstart ASX Miner is the Early Mover in a Growing Domestic Market

Published 08-SEP-2015 09:35 A.M.

|

16 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Almost every single day there seems to be a story in the news about an Australian iron ore miner mothballing operations as the iron ore price continues to hover stubbornly around $50/t...

While companies around Australia are desperately trying to save cash to stay afloat, NSL Consolidated (ASX:NSL) is on the verge of profiting from an iron ore market which is almost totally independent of world markets .

Overlooked NSL has been pigeon holed with every other iron ore miner to date – but for us that presents an opportunity.

NSL is the ONLY foreign company to get a look into a burgeoning domestic Indian iron ore market – a country where steel demand is growing 7% year on year.

As China’s economy undergoes a transition, India is widely tipped to be the next big global growth story for steel makers, and with it iron ore. With years of experience and relationship building in India, NSL is well placed to profit.

Majors Rio and BHP has squirrelled and saved to achieve an iron ore cash cost of $34/tonne, and with the current price at 62% grade roughly $56, they’re making a margin of $22/tonne.

NSL has cash costs of just $23/tonne – producing a low grade form of iron ore where it’s receiving $43/tonne at the mine gate.

That means it margins are roughly $20/t, on par with the biggest of the big boys. At a lower grade too.

How in the hell did it manage to do that?

We’ll run through the reasons this company, which is already in production, has managed to keep its cash costs so low, and is now looking towards a blue sky future in a strong local market.

Oh, and it has just secured a fair chunk of cash to expand, which will see it produce a higher grade product for similar cash costs, yet rake in up to $57/tonne – doubling its net cash flow per annum.

As NSL’s story unfolds in India, it plans to go on and acquire further strong local iron ore projects, which should rapidly boost its production.

At the same time, NSL is a small company, and not without risk – success is no guarantee.

However, in the current iron ore environment, a company seeking to expand production is simply unheard of. And yet, here we are looking at a company doing just that.

Imagine when the Indian iron ore market really takes off?

Re-introducing...

NSL Consolidated (ASX:NSL) is currently on the road talking to shareholders about the next chapter in its growth story, and well it might.

We first brought you NSL in the article Tiny Miner’s First Sales Days Away: Stockpiles Waiting to Be Processed, Delivering Instant Cash Flow last year.

Since that time, NSL has managed to get its 200 ktpa Kurnool beneficiation plant up and running, and sales have commenced.

But lately it’s been kicking some serious goals, and it’s timely that we bought you up to speed on this company imminent expansion plans.

NSL has just secured a $5 million loan which will see it through the scale up of its existing operations at one plant, and the commissioning of another.

It is also currently in active negotiations about further offtake deals for its products, after it tied up recent deals with major steel producers JSW Steel and BMM ISPAT.

Having these two steel producers sign up to buy NSL’s product is a testament to its quality – JSW and BMM are by no means small players...

JSW is India’s leading private sector steel producer and among the world’s most illustrious steel companies. It’s a circa $9 billion global conglomerate, spread over six locations in India and a footprint that extends to the US, South America and Africa.

Meanwhile, BMM’s current and future expanding production of steel can easily absorb 100% of NSL’s fines production.

Before signing off on the offtake deal, both NSL and BMM confirmed the strong alignment of NSL’s iron ore with BMM’s raw material specifications. BMM’s steel complex is approximately 240 kms from NSL’s operation, also in the Karnataka steel producing region.

NSL has also found another non-core product which could help bolster its balance sheet, but more on that later.

Phase 2 Project Economics

Here’s what made us suffer somewhat of a double-take, this is what the Phase two wet plant economics look like for NSL:

Source: NSL Consolidated

Cash costs of $22/t? For an iron ore miner? In 2015?

Somewhere along the line NSL has managed to pull a rabbit from the hat.

We’ll get to just how it did that, but first we’ll give you a bit more of a rundown of what NSL is doing.

The game plan

The canny among you may have noticed that the grades being mentioned in connection to NSL seem... a touch low.

That’s where the beneficiation process comes in – and where NSL starts to grab a first mover advantage in a growing iron ore market.

For some reason, India’s iron ore miners have focused on higher grade iron ore opportunities – a practice known as picking low-hanging fruit, and why not?

A high-grade product means a higher price for ore, and a lesser cost for processing the ore into steel. A win-win, right?

While the rest of India’s miners pick the low-hanging fruit, NSL is quietly building a position in the lower-grade game.

At its three Indian projects, it has its foot on lower-grade iron ore, which it is then bringing up to saleable grade in a beneficiation plant.

Beneficiation plants, both wet and dry, are common facilities in other iron ore producing and receiving countries such as Australia, Brazil, and China, but have not yet made their way to India in any great numbers – until now.

Enter NSL – with its plan to build a beneficiation plant utilising both wet and dry processing techniques to turn its lower-grade ore into ore it can sell for even higher prices than what its getting today.

Source: NSL Consolidated

NSL has already built the phase one plant, which should have an ultimate production capacity of about 680,000 tonnes per year . The company plans to bring in 20-35% grade ore, put it through the dry plant and convert it to 50-55% grade ore, but it’s improving its ore grade all the time.

Total output from phase one is being targeted at 200,000 tonnes per year.

At a $43/t pricing mechanism, NSL is set to generate $3.2 million dollars per year from the first phase plant.

And what’s more, it’s already producing with an offtake agreement in place. As we mentioned above, back in July it announced that it had signed an offtake agreement with BMM Ispat for 200,000 tonnes of existing 57% grade ore.

The sharp-eyed among you may have noticed that the phase one plant is only expected to process up to a 55% grade ore, but the ore underpinning the BMM Ispat offtake agreement is slightly different from the rest...

The ore is just sitting there!

While it was testing its resource at AP23 back in 2013/4, it undertook test mining operations. During the trial, it produced 200,000 tonnes of ore, which subsequently was simply stockpiled on site...

At a slightly higher grade than the average from the project, the ore was simply sitting pretty ready to be fed into a hungry phase one plant.

After technical testing to make sure the ore met BMM’s technical needs, the offtake agreement was signed on a non-exclusive basis, meaning NSL can also talk to other parties in the area about potential offtake.

This stockpiled ore is currently going through the phase one plant and is being sold to BMM.

NSL has one year of production (and subsequent cashflow) already in the bag and has just been funded to ramp up to phase two.

Phase two

Back in August, NSL caught the attention of New York investment firm MG Partners II Ltd , which agreed to put pen to paper on a $5 million loan deal to get production happening at phase one and construct a phase two plant.

The phase two plant will be a wet beneficiation plant capable of bringing ore up to 58%-62%, with capacity of 200,000tpa, and thanks to the funding deal, construction on a pre-fabricated plant has begun in China with an eye to having it on site and commissioned within 12 months.

The phase two plant has been underpinned by offtake agreements with JSW Steel and BMM Ispat , meaning that all NSL needs to do now is actually build the thing and let the revenue flow.

It has the technical capability, it has the resource, and it has the money in the offing.

One of the key reasons MG Partners decided to invest in the project was the strong market fundamentals in one of the largest emerging players in the world...

Why India?

One of the key reasons we have been following NSL for a while is because it’s the only Australian player in the Indian iron ore market, a market which is tipped to more than triple in coming years.

The Indian economy more broadly has a GDP of $1.3 trillion, making it the eighth largest economy in the world. However, on a price parity basis which recognises the low cost base in India, its GDP rises to $3.8 trillion.

In fact, on price parity terms it’s only behind the US and China – and we all know the Chinese growth story is facing challenges at the moment.

Its consumer market is ticking along nicely, with every sector within India’s consumer market growing. This makes India far less vulnerable to external shocks and pressures than other emerging markets.

The country’s steel ministry announced earlier this year that it would aim to have 300 million tonnes of steel production capacity by 2025, meaning more infrastructure will be needed in the country to help it hit this target. All good news for NSL.

A recent Ernst & Young report on the Indian steel sector recently noted that the government was showing signs of coming to the party. “Government investment in public infrastructure projects, including dedicated freight networks and ongoing rapid urbanization, will underpin this growth,” it noted.

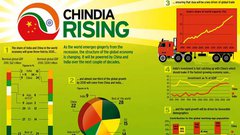

Most of the iron ore and steel produced in India is consumed domestically, as shown by the chart below.

Source: NSL Consolidated

This means that the market for NSL’s Indian iron ore production is speaking to a rapid urbanisation story.

In recent years, you’ve seen what’s happened in China with its own domestic growth story. This has equated to more building in urban areas as a rising middle class demand better housing, more often than not underpinned by steel.

A similar story could be about to play out in India, and NSL is there with an early stage position and set to take advantage of it. At the same time, operating in India can present political risk, so NSL is still a speculative investment.

To really appreciate this, take a look at the below figures – As you can see, India has a lot of catching up to do when it comes to steel consumption.

Source: NSL Consolidated

At the moment, estimated steel consumption per capita is 61kg per person per year, but with rapid urbanisation underway this could be set to grow at a rate of knots.

NSL is placing itself front and centre to service this demand by supplying domestic iron ore to Indian steel makers.

One of the other reasons why India is an attractive destination to do business in is because it is a low-cost environment.

It’s not just because there are lower wages, but it’s also because it’s easier to get around than in Australia.

Those who have tangled with the streets of Delhi and lived to tell the tale may be a touch mystified by that statement, but compared to Australia, it’s easier to operate an iron ore mine in India.

In Australia, you have to put a workforce on a plane in Perth and fly them all the way to Tom Price, 1,470km away.

In India, the workforce is mostly local – giving a smaller player such as NSL a look into a space which is normally a scale game.

With its core projects funded with offtake agreements in the bag, NSL is starting to think a little bit bigger too.

Operations at a Glance

At its core, NSL is an iron miner taking advantage of a huge market opportunity in India by playing in a space where others, somewhat inexplicably, won’t – by bringing lower grade ore up to snuff using the beneficiation process .

It is concentrating on three key mining licenses in the Andhra Pradesh region of India, an internationally recognised iron ore province.

Source: NSL Consolidated

Let’s delve a little deeper into NSL’s operations:

AP23 deposit

This is a 73 hectare mining lease in the Kurnool district, only 13km from NSL’s existing stockyard, 5km from a national highway and 13km from rail.

As any seasoned iron ore investor will tell you, rock is only half the battle with markets and infrastructure proximity playing a key role in whether a rock-hunter will become a rock star or not.

While it hasn’t yet defined a resource at the lease, it does have some technical work under its belt with an initial exploration target of 38Mt to 95Mt with an average grade of 20-55% iron ore.

Kuja

The Kuja project has mining approval for up to 331,000 tonnes per annum of iron ore.

While this is merely an aspirational target, it gives you some idea of the sort of potential NSL sees at the project. After all, why go through the bother of applying for that much production if you don’t intend to use it?

It has access to both established road and rail infrastructure, and links directly to the highway to the Krishnapatnam Port, which is the closest point of departure for bulk exports from Andhra Pradesh, around 330km away by road.

The road also connects to two rail sidings that have infrastructure for loading iron ore to trains, which are approximately 18km and 30km respectively by road from the mine gate. It is approximately 460km from the rail siding to Krishnapatnam Port by rail.

It’s also right next door to NSL’s beneficiation plant, where the Phase 1 production plant is located, and it is here that NSL have been refining their beneficiation capabilities.

It’s also at this site where the Phase 2 production plant will be located.

Mangal

Right next door to Kuja is Mangal, which has mining approval for 500,000 tpa over five years. Again, this is a maximum figure, but gives you an idea of what it could be pulling out of the ground.

Mining plans approved, to 500,000 tonnes per annum over the 5 year period of validity for the Mining Plan.

Again, it has infrastructure on hand, and has done technical work ups on its ore, with 213 bulk samples taken during a trial mining phase.

The material was mined, crushed and screened under the direction of geologists. It had an average grade of 38.3%, with a range between 20% and 60%.

All of the above assets are NSL’s – and all are operational.

NSL’s next growth phase

While NSL has plans for phase one and two at Kurnool well under foot, the company is now building toward its next growth phase:

Source: NSL Consolidated

NSL is targeting potential acquisitions, and you don’t do that if you’re not confident in your core business.

It’s also talking about two main things going into the future...

AP14

In Telangana, the neighbouring state to Andhra Pradesh, NSL has got its foot on a magnetite project which it’s been quietly firming up.

In a coup for the company, the project has been declared a “Project of National Significance” – pointing to the relationship NSL enjoys with the government and testament to the quality of the project.

The Indian government have committed to assisting the project move through the bottlenecks sometimes associated with major projects in the country – so it’s a great box ticked for NSL.

The “Project Monitoring Group” has been set up by the Prime Minister’s Office with the Government of India, to proactively pursue new major infrastructure projects and any stalled projects to ensure that the projects are commissioned on time.

The PMG restricts its interest to projects deemed critical to the National Interest or involving more than 1,000 Indian Crores (approximately A$180 million) of total investments, so having NSL’s project elevated to this status will assist in bringing the AP14 project to life.

The target mineralisation at AP14 consists of Banded Magnetite Quartzite, which from surface mapping and geomagnetic surveys, covers between 50% and 70% of the project area.

NSL has undertaken both physical and geomagnetic surveys, and has an exploration target of 134 million to 377 million tonnes of magnetite, at grades ranging from 25% to 50% iron.

Contained within this exploration target there exists potential for a high grade core of Direct Ship Ore (DSO) quality enriched magnetite, with estimates from 5 million to 10 million tonnes with a grade range from 55% to 65% Fe.

While it’s all still conceptual in nature, further exploration at the project could provide further blue sky potential for NSL. And as the cash starts coming into the company’s coffers, it’s likely they will look to progress this project as a priority.

NSL’s mystery product...

In the past six months or so, we’ve noticed that NSL has started to talk about a mystery product – which has continued to pique our curiosity.

Especially since its secured purchase orders for it, and it will create an additional revenue source for the company.

So what the heck is it?

When it was mining at its projects, it started to notice that it was bringing up rocks with a special blend of iron, silica, and alumina.

This blend is seen as vital to the performance of the furnace and quality of finished cast iron when it is being produced.

In August, NSL received a purchase order for 100 tonnes of the specialised mix from Srikalahastri Pipes Limited for a trial quantity of sized lump iron ore for use in their pipe casting division.

Srikalahastri is a part of the Electrosteel Group.

This cross India group is focussed solely on steel and value addition, and has installed capacity in excess of 2.5mtpa of hot metal, combined with numerous other value addition operations, focussed heavily on steel pipes and cast products.

So if the client is happy with the initial offtake – NSL could potentially open up another market for a product not currently generating revenue for the company...

We will be keeping a close eye on developments on that one.

The final word

NSL has now has funding under its belt and offtake agreements in the bag, which are needed to build its core business, and it’s starting to think about some blue sky ideas including marketing of new products and magnetite exploration.

As you read this, NSL is generating revenue from its stage one plant giving it a firm footing from which to grow.

It’s even talking quietly about acquisitions...

NSL has managed to keep cash costs low to the point where it is price competitive with the likes of Rio and BHP which have the benefits of scale, using a canny market strategy to take an early-stage market position right under the noses of local operators.

NSL has plugged into one of the bigger commodity growth stories in the world, with steel demand in the country set to skyrocket on the back of the urbanisation of one of the largest economies in the world.

It has a stellar relationship with the government, to the point where one of its major projects has been declared a project of national significance. Given the size and scale of India, “significant” may be underselling it...

Whilst NSL is still in the early stages of its development, the company remains a speculative investment.

In any case, it’s shaping up to be a big couple of months as NSL go about finalising its Phase 2 plant – and with it, even more cash flow set to come its way...

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.