Our week in Cape Town, South Africa, for the Mining Indaba Conference

Published 10-FEB-2024 10:00 A.M.

|

18 minute read

We heard someone whisper on the plane...

“It’s very hard to move from explorer to producer.”

A truism, sure, but it was just the beginning.

Clearly, there was a “mining guy” in the aisle over.

On a quick glance around, at least a couple of them.

And more everywhere you looked...

As everyone descended on Cape Town, South Africa, for the annual Indaba conference you could see why there was mining chatter all around.

Indaba is one of the largest mining conferences in the world, and the premier mining event in Africa.

Mining companies, investors, governments, financiers and other stakeholders in the mining industry meet to network, make deals, and discuss opportunities and challenges in the mining sector in Africa.

We have 10 companies in our Portfolio with resource projects in Africa - we think the continent has incredible promise.

And hopefully one of them will eventually become a producing mine.

The pantheon of +$1BN market cap mining companies is rarefied air that few ascend into.

But despite the difficulty in achieving this feat, here everyone was, having a crack.

Indaba is a powerful force to behold.

Thousands of business types in suits (us too begrudgingly), hurriedly talking on the phone, lining up for things, having quick chats, then rushing off.

Everyone has a deal or a purpose to pursue, and everyone has some form of connection, however tangential.

And everyone is in the same spot at the same time.

Government ministers speaking, experts pontificating and eager onlookers keen to learn and get an edge.

Lots of private resource projects looking for funding, and finance brokers looking to fund them and list them on a stock exchange (preferably the ASX).

With exploration and early stage sentiment ebbing, it seemed asset prices have become very attractive for those patient enough to wait for the next bull market.

We certainly picked up a few intriguing insights at the conference...

And even ended up on stage ourselves to help judge a resource juniors pitch battle.

But the really interesting insights came at the events and dinners outside the conference...

This is where the serious players can usually be found, if you can finesse your way into the right places of course...

Major mine financiers aren’t usually just “knocking around” the conference floor.

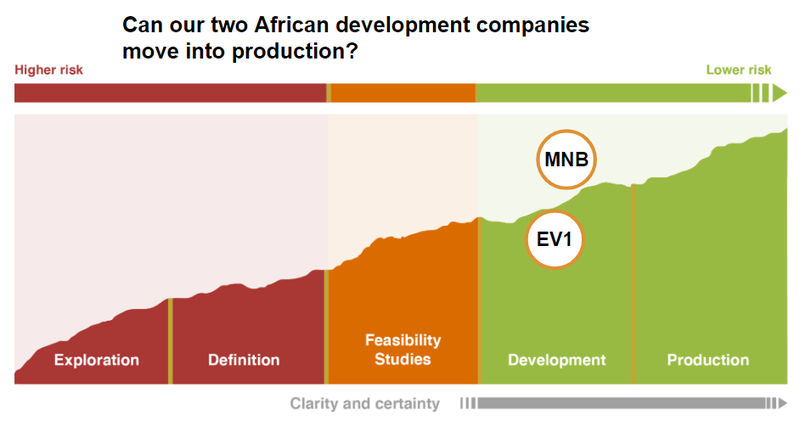

Now that a couple of our Investments have reached “mine finance stage” we were interested to learn about the process for obtaining finance to get a mine built.

After years of Investing in exploration, we are hoping we will soon own a couple of producing mines in our Portfolio - and two of our nearest term candidates are located in Africa:

Mine finance usually runs into the hundreds of $ millions - not the $3M to $5M cap raises to fund more drilling or studies that we are used to.

We (somehow) managed to get chatting to a couple of serious mine financiers, in social settings outside the conference.

Turns out they relax once they figure out you aren’t a junior mining CEO that's going to hassle them for hundreds of millions of dollars.

And they kindly shared some of their insights into the mysterious (to us) world of later stage mine financing.

(Can you imagine writing a $250M cheque to build a mine?)

Finance to build a mine is usually a mix of equity and debt.

We also chatted to some “debt advisors” who help resource juniors secure the usually equally large debt portion of the financing to build their mine.

After landing in Cape Town, our first stop (after the obligatory first night of “off-conference” events) was to stop at Indaba’s “little brother” - the 121 conference for mining juniors.

121 is where junior mining companies “speed date” with sophisticated investors and financiers.

While on-market buying has cooled for mining juniors in the last 12 months, it certainly wasn’t evident at the sophisticated end, with the 121 conference sold out and turning away requests to buy tickets at the door.

It looks like the “sophisticated and patient money” is also on the hunt for some low entry points during the current down cycle.

For the second year in a row, we witnessed Phil Hoskins from Evolution Energy Minerals (ASX: EV1) grind through two full days of back to back meetings.

(He showed us his 16 hour a day meetings schedule, including pre and post event meets).

We also spent a bit of time with Joe Graziano from Tyranna Resources (ASX:TYX).

Joe was in an upbeat mood and relaxed - makes sense given TYX have recently secured a massive +$31M in financing and are now drilling their lithium project in Angola.

We can’t wait to (hopefully) see some great hits from TYX’s upcoming assays, they’ve been turning up some chunky spodumene so far.

Spodumene could mean lithium, and even in a down market - this will be important.

Over at the main Indaba conference we caught up with Lindsay Reed from Minbos Resources (ASX:MNB).

We eventually got onto him, as he was ducking out regularly to take meetings outside the conference.

We also saw Heavy Minerals (ASX:HVY) chairman Adam Schofield (HVY has a lesser known, but still sizable mineral sands project in Mozambique) who was busy mixing with the various royalty funds that were in attendance.

Uranium, gold and graphite were the most popular topics of discussion.

We noticed there were a LOT of car companies around too - no doubt on the hunt to secure battery metal supply.

Car companies need to think in decades, not years - so are likely not deterred by the current soft patch in battery materials at the small end of the market.

We heard rumours of an event where car makers and battery metals miners all get into a room to meet and mingle - this one wasn’t open to the public so we couldn’t peek in.

Most African countries had a booth, Angola (MNB and TYX) had the biggest booth again this year.

A key part of a country booth is showing off the country's willingness to encourage mining investment and show off existing mines and available infrastructure, as you can see here at the Gabon booth:

We learned that infrastructure is key when it comes to later stage financing.

Sidebar: Germany had the largest floor space at the conference - it was interesting to see.

We know Germany is one of the countries that is most keen for the energy transition and their carmakers are likely very hungry for critical minerals and the projects that produce them.

We also got to see lots of cool mining and exploration technology - including testing out an XRF gun (the thing that exploration companies use to get a rough estimate of mineral grades in core samples on site before assay results).

We attended an interesting session on how African governments are maturing on how to attract and retain mining investment.

With increasing knowledge and confidence about mining, resource deposits and investment frameworks, African governments are better able to provide the stable regulatory environment required to best attract junior miners and actually get mines built in a true win-win situation for the country, the local community, the mining company and its investors.

In terms of the market sentiment for juniors and later stage resource companies, there was no real surprises.

Later stage companies are positioned to run when commodities come back into favour.

There are bargains around in exploration - there is still interest in explorers but it seems to be from bigger funds/sophisticated investors who will wait for a cap raise to take a position at grotesque terms.

Given the current tough market conditions at the small end, over the next few months we will be ramping up new Investments while share prices are beaten down.

How a mine actually gets built - mysterious financiers circling

Exploration is one thing - drilling in the hope of finding a deposit of a valuable commodity.

Exploration drilling can cost less than a million dollars (depending on how many failed attempts are made and which country a company is in).

Let us not forget that, Latin Resources (ASX: LRS) had $643K in cash before drill rigs arrived on site at its major lithium discovery in Brazil.

It doesn’t take much for explorers...

And this is an area of the market we have been Investing in for a long time and are familiar with.

Actually building a mine is a whole different game.

Once a discovery has been made, drilling has defined a JORC resource, metwork tests have determined extraction economics, and the company has completed feasibility studies up to and including a “bankable feasibility study”.

Now the company knows in detail exactly how much $ they will need to build and operate the mine and how much profit it is forecast to make over its life.

Then it’s time for the company to find people willing to stump up the hundreds of millions required to build the mine...

One of the main benefits of Indaba is that it allows people to meet who otherwise wouldn’t.

Much of the action and deal making takes place away from the conference, and some particular functions before the conference kicked off, we had a chance to chat with some serious financiers.

Some were a touch reserved, and many wouldn’t mention which funds they worked for, but their knowledge was very impressive.

One of them mentioned offhand that his firm had written a US$250M convertible note for a company to put it into production.

That’s some serious firepower.

And it's also what many later stage small cap companies dream of.

We had a chance to pick their brains on some projects, and suffice to say, their due diligence process is long and extensive.

There are many resource companies out there at PFS or BFS stage looking for financing.

We were surprised that most of the later stage financiers we spoke to already knew about nearly every company we threw at them... and already knew the CEOs.

There are a huge host of projects all over the world vying for these financiers' attention - and one of the things that they said rang true...

For these later stage financiers, it's not the projects you DO invest in that matter, it's the ones you DON’T invest in that make the difference.

Very different to the “spray and pray” approach for investing in early stage exploration.

Which speaks to how deep their understanding of what makes a mine profitable.

The financiers also said that later stage companies would run very hard when commodity prices come back - which is to be expected, but it was nice to have it confirmed.

The trick is putting yourself in the best place at the right time, they added.

After hearing all this, it re-strengthened our desire to add more later stage companies to our Portfolio.

Most companies that need a large sum of cash to build a mine will use a mix of equity (raising money by issuing new shares) and debt (borrowing cash).

We also met with some debt advisors that help companies secure the debt portion of their financing.

Debt advisors know all the banks and lenders out there who specialise in loaning money to build mines.

The words of wisdom they had for us was to keep a close eye on debt terms - not all debt is equal, and having a CEO who has skin in the game and can hold firm on negotiating terms is critical to get a good deal.

They told us some examples of debt deals that they had seen that were overly aggressive for the borrower and would put too much pressure on the company, increasing the chance of failure.

The debt portion of mine financing is usually expected to be repaid after a few years of the mine's operation, from revenue generated by the mine.

Catch up with MNB

We caught up with MNB Managing Director Lindsay Reed at Indaba.

MNB is currently building a phosphate mine in Angola. Phosphate is a key ingredient used to make fertilisers for food production.

Lindsay looked pretty stoked with whatever had happened at the meeting he had before us.

We reckon MNB is going to be our first ever Investment that moves to a successfully producing mine.

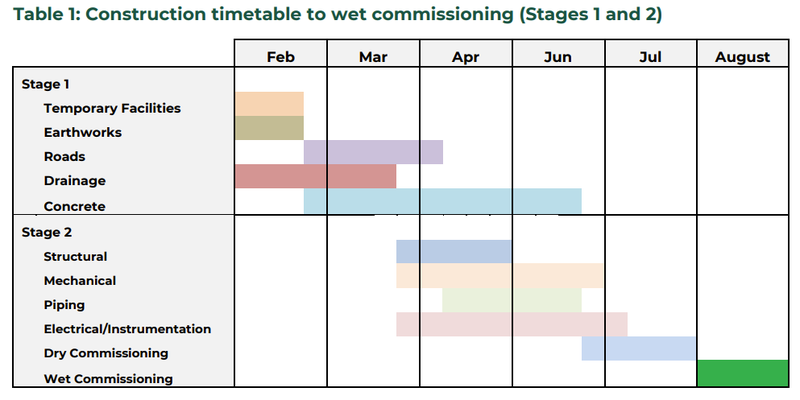

MNB has a relatively low capital expenditure to build their mine, with about US$20M remaining to finish the build.

A couple of weeks ago MNB released a schedule which shows first production this year:

(Source)

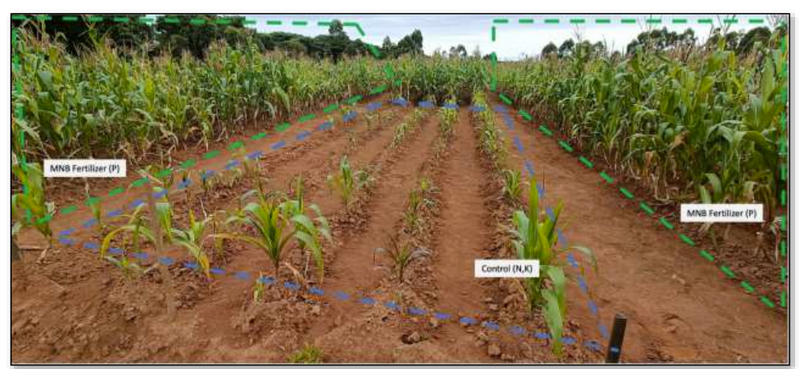

Last week MNB also released an update that field trials of fertiliser were showing outstanding crop productivity increases (MNB’s phosphate was used in both the outer sections of the below image, which are clearly growing better than the benchmark base section in the middle):

(Source)

After last years Indaba we travelled to Angola to visit MNB’s projects and see it all with our own eyes - you can read the about our MNB site visit here:

On the Ground in Angola: Our MNB Site Visit

A hive of activity - 121 is where juniors gather

On Monday we headed to the 121 Conference which served as an excellent prelude to what we would see across town at the sprawling Cape Town International Convention Centre.

It sits alongside Indaba at a separate venue.

121 is a well oiled machine of a conference if you Invest in small cap African companies like we do.

The junior end of the mining space has been soft for the last few months... but looks like 121 attendees didn’t get the memo.

121 was PACKED:

Despite a downbeat market on the charts for small caps, the hum of 121 told a different story.

People were moving quickly from booth to booth, you could sense urgency and enthusiasm.

It’s like efficient small cap speed dating that actually works.

121 is where assets are discussed, financiers hover and perhaps even a “whale” offtaker appears if you’re lucky.

The “whales” generally keep a low profile though, we might add.

First thing we did was stop in to see Evolution Energy Minerals (ASX: EV1) Managing Director Phil Hoskins - we’ve written about the big moves the company is making in the graphite space recently.

EV1 has an advanced stage graphite project in Tanzania, and has just signed a deal with the world’s largest anode maker, BTR, to help take EV1’s graphite into the US market.

Phil pointed to a list of meetings going over two pages - Phil is one of the hardest working MD’s we know.

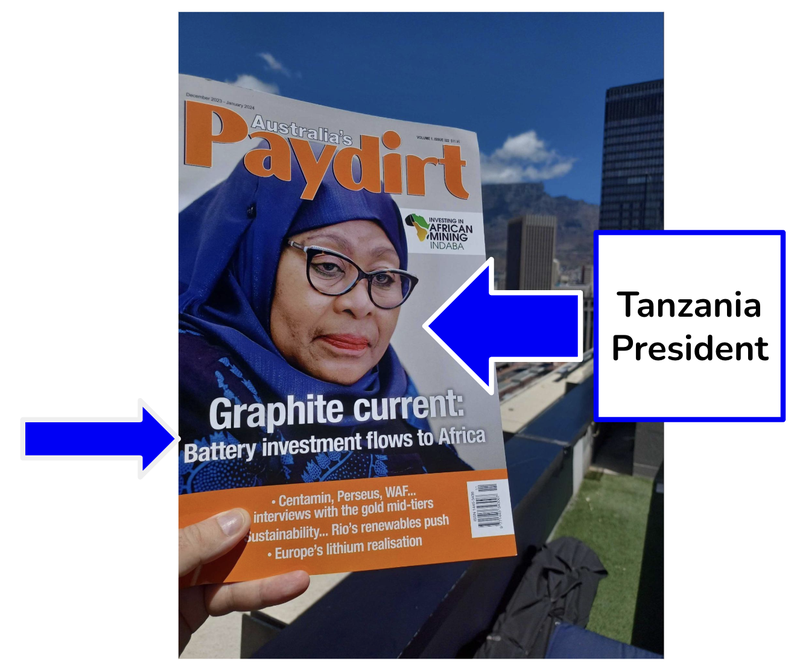

He was upbeat about the future, and Tanzania was mentioned many times throughout the trip as a great place to do business.

(Even from people without projects in the country.)

A quick glance at a copy of the Paydirt magazine picked up at Indaba confirms this - Tanzania’s president on the cover says it all:

Phil of course, has met the Tanzanian president at the signing ceremony for EV1’s framework agreement which enshrines EV1 in the country’s mining system:

For the full story on how EV1 is leveraging the graphite wars between US and China read:

EV1 Acts to Thaw US-China Battery Spat. Supply Chains Intact

We’re big believers in EV1, and the graphite thematic as a whole.

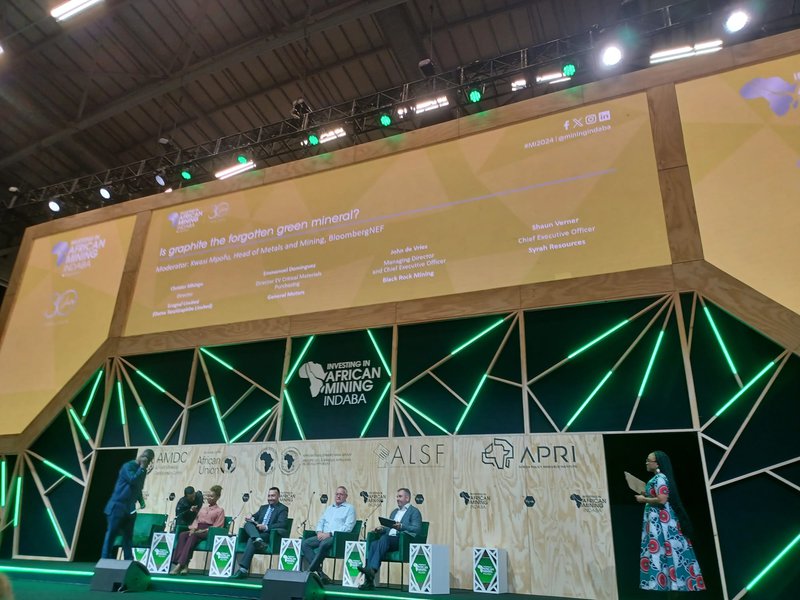

This is why on Wednesday we made sure to attend a session at Indaba called “Is graphite the forgotten green mineral?”.

Here’s the story on that...

Is graphite a dark horse in the battery materials race? A major US carmaker really wants to buy

One of the things that Indaba does very well is bring together a diverse range of industry participants, from vendors to explorers, developers, producers and end users.

A big stakeholder this year was carmakers.

And the one thing that keeps every carmaker awake at night is security of supply.

That was expressed at this session we attended:

Looking at the agenda ahead of the conference one event really stood out to us.

“Is graphite the forgotten green mineral?”

It was a panel hosted by the Bloomberg New Energy Finance Head of Metals and Mining - a solid moderator.

And then in between three graphite executives - was the General Motors (GM) Director of EV Critical Materials Purchasing Emmanuel Dominguez.

General Motors is the largest carmaker in the US, after reclaiming its spot from Toyota and has big EV plans.

It was an interesting ensemble - and GM’s representative didn’t disappoint - Dominguez’s job is to move his company into the supply chain.

We’ve seen GM make a flurry of offtake deals before:

- Lithium offtake with Lithium Americas, January 2023

- Manganese offtake with Element 25, June 2023

- Nickel offtake with Queensland Pacific Minerals, October 2022

Two of these were Australian listed companies - so there is a good precedent there.

So putting two and two together, you can see why GM was in the room.

GM wants graphite.

Graphite might be considered forgotten by many, but for us it is one of our biggest macro themes, and if things change in 2024, the market may be caught off guard in a big way.

Bubbling beneath the surface, we think graphite is a battery materials dark horse.

A GM graphite offtake would certainly spark market interest for EV1.

Indaba - Junior Mining Pitch Battle

We were invited to the judging panel for the grand final of the indaba pitch battle to find the best exploration project in Africa.

These were the other judges:

- John Meyer, Partner and Mining Analyst, SP Angel

- Bereket Berhe, Managing Director and Mining Analyst, Beacon Securities

- Jonathan Cordero, Head of Corporate Development, Eurasian Resources Group

And the five companies that pitched:

- Chilwa Minerals (mineral sands, Malawi)

- Adavale Resources (nickel in Tanzania, uranium in Australia)

- Sanu Gold Corp (gold in Guinea)

- Alpha Exploration (gold/multicommodity in Eritrea)

- Elevate Uranium (uranium in Namibia, Australia)

Five junior companies pitched, each was exploring for a different commodity, at different stages of exploration and in different countries.

Just like Investing in exploration right now, the choice was very difficult.

Do you go for the “in favour” commodity like uranium but where the share price may have already run, or do you go for the “out of favour” commodity like nickel where the company is trading at all time lows and patiently wait for the market to turn.

We have found it’s good to have a mix of both.

In the end Alpha Exploration was crowned the winner, given its multiple high quality exploration projects and its team’s previous success in bringing projects from exploration to a producing mine in Eritrea

Next Stop... DLE conference in Arkansas and PDAC

The next stop on our trip is the Lithium Innovation Summit in Arkansas, US.

Here, all the major lithium brine players in the region will be presenting on the latest in lithium extraction from historical oil fields in the Smackover.

Over the last 12 months our small cap Investment Pantera Minerals (ASX:PFE) has been busy, acquiring old oil fields in the Smackover that have no more oil, but are rich in lithium brines.

We will visit the PFE site as well as the Lithium Innovation Summit.

At the summit some of the biggest names in the region will be speaking, including: Standard Lithium, Exxon, Albermale and Tetra, as well as the governor of Arkansas, Sarah Huckabee Sanders.

After Arkansas we make our way to PDAC in Canada.

PDAC and Indaba are two of the biggest mining conferences on the yearly calendar.

Keep an eye out for our write up on the PFE site visit as well as our take on the PDAC conference.

Maverick Minerals IPO is Open

This week we noticed that the Maverick Minerals IPO got some coverage in the AFR.

(Source)

For those who missed our weekend email last week - Maverick Minerals is a spin out from one of our existing portfolio companies - $410M Latin Resources (ASX:LRS).

As mentioned in last week's weekend email, we are participating in the Maverick Minerals IPO.

LRS will be 16.2% shareholder in MVM.

MVM plans to list on the ASX on March 6th (indicative date).

For full details see the MVM IPO prospectus.

To bid into the MVM IPO click here

Make sure to read the prospectus in full before you bid.

What we wrote about this week 🧬 🦉 🏹

88 Energy (ASX: 88E)

This week 88E confirmed that construction works had commenced on a drill pad for its Hickory-1 flow test.

Last year 88E drilled the Hickory-1 well and in November declared a discovery across one of the six reservoirs intercepted during the drill program.

In the next few weeks, 88E will be kicking off a flow test where it will be aiming to show the project can produce at commercially viable flow rates.

In our note this week, we setup our expectations for the flow test and detailed what we think success will look like for 88E.

Read: 💦 88E Found Oil. Does it Flow? We will Soon Find Out.

Sarytogan Graphite (ASX: SGA)

This week SGA confirmed that its graphite can be used to produce lithium ion batteries.

SGA put out test results for batteries that were produced using SGA’s graphite - the results showed that SGA’s graphite performed at a higher level than other synthetic graphite equivalents.

After this weeks news, SGA ticked off a major milestone that we think sets up the company in a unique position given its relatively low market cap.

Read: 🔋SGA’s graphite tested in batteries - consistently outperforming synthetic graphite

Quick Takes 🗣️

MAN: MAN receives drill permits for US Lithium project

LNR: LNR sampling for lithium next to one of Australia’s biggest mine

NHE: NHE lab results increase net pay by over two-three times

GGE: GGE sidetrack well design complete

NTI: NTI ASD patients still being treated after 90 weeks

PUR: PUR drilling for lithium brines in South America’s lithium triangle

MAN: MAN sampling for uranium <5km from producing mine in the US.

HAR: HAR ranks more RC drill targets ahead of drilling in mid-February

TG1: TG1 sampling results from WA lithium project

EXR: EXR releases lab results from QLD gas project

PFE: PFE increases lithium acreage in the Smackover, USA

BPM: BPM drilling next door to $1.8BN Capricorn Metals

Mainstream News from The Future Money:

Silver Lake and Red 5's $2.2BN Gold Rollup

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.